Open Banking Payments in 2026: Insights from Fire’s Webinar

Article snapshot

Key insights from Fire’s latest Open Banking webinar.

A practical look at payment initiation, Fire’s end-to-end service, and the evolving open banking landscape.

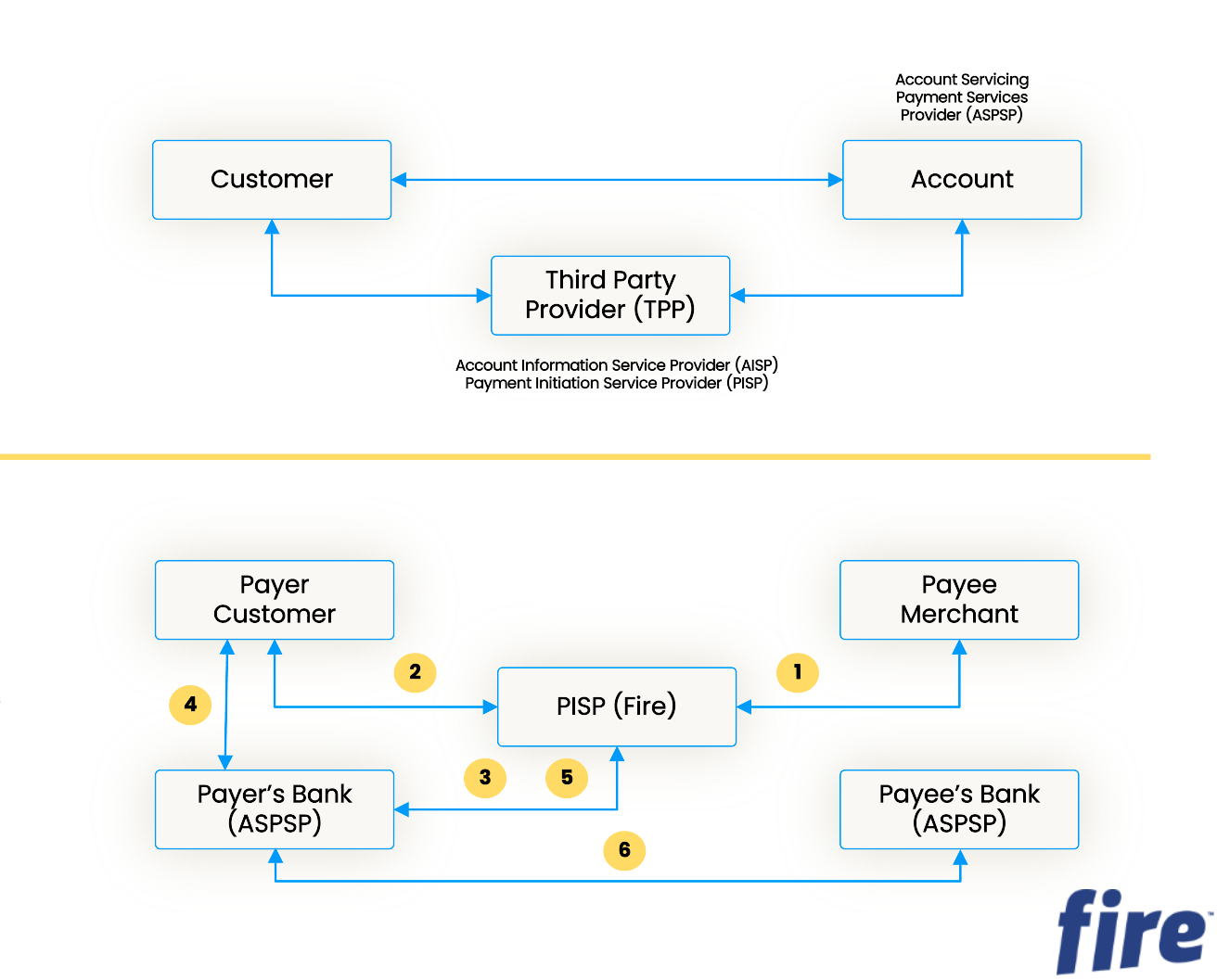

What is open banking?

Open banking is a regulated framework that allows customers to securely share their account information and initiate payments through authorised third-party providers (TPPs). In practice, this allows businesses to integrate directly with a customer’s bank account to offer fast, secure, and data-rich payment experiences.

Since its introduction in 2018, open banking adoption has grown steadily. While account information services (AIS) remain an important part of the ecosystem, much of the recent innovation is focused on payment initiation services (PIS). These services enable businesses to request and collect payments directly from a customer’s bank account in real time, securely, without manual entry of payment details.

Fire is regulated as both an AIS provider and a payment initiation service provider (PISP). Our focus is on delivering value through PIS, helping businesses streamline payment collection, improve cash flow, and enhance the customer payment experience.

Open Banking Payments

Payment initiation

Payment initiation enables a business to request funds from a customer’s account. This process typically involves:

- The payer receiving a payment request via a deep link, QR code, NFC, or other channel.

- The payer selecting their bank (the account-holding institution, or ASPSP) and authenticates the payment request.

- Fire generating a single-use token to initiate the payment.

- The payer’s bank executes the transfer directly to the merchant or an intermediary account.

This flow allows businesses to accept payments in a secure, standardised way while providing consumers with flexible options that suit their journey, whether online, in-store, or on mobile.

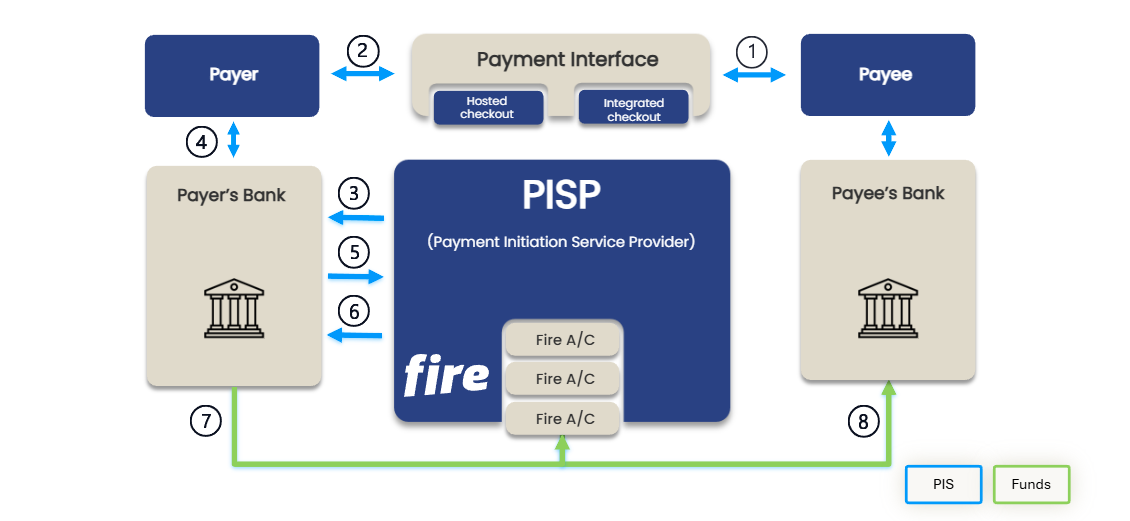

Fire Open Banking Payments: PIS and collection, reconciliation and settlement

Fire offers a full end-to-end service that goes beyond payment initiation, providing collection, reconciliation, and settlement for open banking payments. Key elements include:

Collection

Payments are collected into Fire accounts. Multiple accounts can be used to segregate funds by merchant, fundraising campaign, or customer segment. This simplifies reconciliation and allows flexible onward settlement.

Reconciliation

Each payment includes rich data, which can include order IDs or product references, enabling instant and accurate matching to internal records. Manual effort and errors are reduced, while maintaining oversight of payment status.

Settlement

Collected funds can be settled to external bank accounts as needed, or disbursed across multiple accounts, supporting complex flows such as platforms, marketplaces, or third-party distributions.

Customisable payment experiences

Fire provides hosted or integrated checkouts, which can be fully branded for consistent customer experience. Payment request links can be distributed via QR codes, deep links, embedded in apps, or via NFC tags, offering convenience and flexibility.

Event-driven Webhooks & real-time confirmation

Webhooks can be configured to notify businesses when payments are authorised or settled, supporting automated workflows. Real-time confirmation of funds allows businesses to release goods or services confidently without needing to wait for the next settlement cycle.

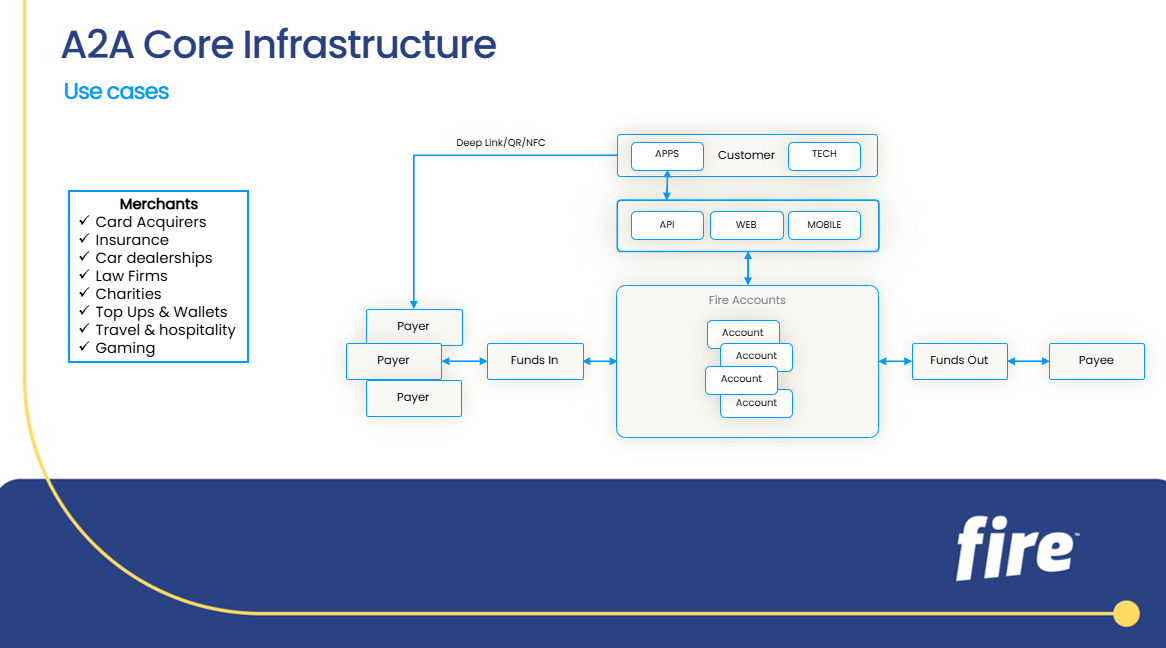

Use cases: how businesses are using Open Banking payments

At the webinar, we highlighted some of our key clients and shared practical examples of how these organisations have integrated with Fire to streamline their payment flows.

Charities

Charities can set up multiple collection accounts for campaigns or locations, making it easier to manage donations. Irish Guide Dogs, which supports people with visual impairments across Ireland, uses Fire’s Open Banking Payments to allow donors to pay quickly and securely via QR codes on marketing materials, at events, or even on cycling jerseys. The approach provides a simple donation experience for supporters while offering a more cost-effective alternative to traditional payment methods, helping the organisation maximise the value of every donation and scale fundraising initiatives efficiently.

Insurance

Open banking payments give insurers richer reference data for automatic reconciliation, reduce errors from manual entries, speed up settlement, and lower processing costs, improving efficiency across premium collection workflows.

Acquirers

Fire works with payment acquirers to bring open banking payment methods to market, enabling them to offer account-to-account payments alongside cards. This helps acquirers respond to merchant demand for lower-cost payment options. Fire provides the underlying infrastructure for collection, reconciliation, and settlement, and works with acquirers to support operational requirements such as tailored reporting and payment workflows.

Travel, hospitality, and gaming

High-volume transactions benefit from real-time confirmation and secure, PCI-free payment flows. Consumers can pay via QR code, deep link, or embedded checkout, improving conversion and reducing friction. Gaming merchants such as Gr8Odds and Fitzwilliam Sports have integrated Fire’s platform to streamline payment flows and improve operational efficiency. By leveraging open banking and automated reconciliation, these businesses reduced manual work, shortened settlement cycles, and provided players with secure, card‑free payment options.

Marketplaces and platforms

Funds can be automatically routed to multiple merchants or recipients, with full transparency and reconciliation built into the system.

Horizon scanning: the evolving open banking landscape

During the session, the Fire team looked ahead to how open banking is continuing to evolve across Europe and the UK.

Instant payments were a central theme. With SEPA Instant expanding across Europe and Faster Payments well established in the UK, near-instant settlement is increasingly becoming the standard. As regulatory mandates bring more financial institutions into scope, real-time account-to-account payments are expected to become the norm.

The team also discussed variable recurring payments in the UK, which will allow merchants to initiate repeat payments under a single authentication. This opens new use cases for repeat payments such as subscriptions, utilities, and other ongoing services using open banking infrastructure.

Emerging person-to-person and person-to-business solutions, such as Zippay in Ireland, Wero in Germany, and Bizum in Spain, were highlighted as examples of how mobile-first account-to-account payments are becoming more accessible and embedded into everyday payment journeys.

Webinar Q&A: questions from attendees

The session concluded with a Q&A covering implementation, timelines, and practical considerations. Key questions included:

What is the biggest challenge for businesses adopting open banking?

One of the biggest challenges is consumer awareness and familiarity. Many customers are still learning what open banking is and how it works. Once a consumer uses it for the first time, however, they tend to become more comfortable using it again.

Businesses can help accelerate adoption by clearly communicating the payment option during checkout and designing the payment flow in a way that encourages customers to try it. In some cases, merchants that actively promote open banking payments have often seen strong uptake.

Can businesses accept payments from overseas?

Fire’s Open Banking Payments currently focus on bank connections in Ireland and the UK. As a result, open banking would typically be used for payments from customers with bank accounts in those markets. However, international payments can still be accepted through SWIFT transfers into a Fire account. Businesses can generate SWIFT payment details within their account to receive international payments in currencies such as euro or sterling.

How does the cost of open banking compare with card payments or bank transfers?

Open banking payments are typically much lower cost than card payments, because they do not involve card scheme fees such as interchange charged by networks like Visa or Mastercard. Costs are generally comparable to standard bank transfers, as both operate on bank transfer rails. While pricing can vary depending on the specific implementation or use case, most businesses see clear cost savings compared with cards.

If a business mainly uses cards or bank transfers today, where does open banking make the biggest difference?

Open banking tends to deliver value in three key areas:

- Cost – lower fees compared with card payments.

- Data – richer transaction information improves reconciliation and reduces manual work.

- Speed – faster settlement times improve cash flow.

For example, with traditional card payments businesses may wait one to three business days for settlement. With open banking, payments can be confirmed immediately and, as instant payments expand, funds can arrive within seconds.

What kind of cost savings can businesses expect compared with card payments?

The exact savings depend on the business’s existing merchant service rates and industry.

However, in most cases open banking payments are significantly cheaper than card payments, especially for high-value transactions where card fees can be more noticeable. Businesses typically evaluate savings by comparing their current card processing costs with open banking transaction fees.

Are variable recurring payments available in Ireland?

Not yet.

Currently, open banking payments in Ireland require customer authentication for each transaction. Variable recurring payments, where a customer authenticates once and allows multiple payments over time, are gaining traction in the UK.

We do see Variable Recurring Payments being developed in Ireland, but this is likely to be a medium to long-term development rather than an immediate change.

What should businesses be thinking about now to prepare for the future of payments?

Many new payment innovations, including instant payments, open banking payments, and other account-to-account solutions, rely on systems that can connect to accounts programmatically. Businesses that implement API-driven payment infrastructure today will be better positioned to support new payment methods and automation capabilities in the future.

When will instant payments be available?

Credit institutions within euro area member states were required to implement SEPA Instant in 2025. This mandate will extend to e-money institutions and payment institutions by July 2027.

How is payout automation expected to evolve, especially in relation to SEPA instant?

Demand for payment automation is growing rapidly, driven by rising consumer expectations. Businesses adopting integrated, automated solutions can take full advantage of instant payments, streamline flows across suppliers and payees, and differentiate their offerings. Fire aims to help businesses unlock these opportunities.

–

If you would like to learn more about open banking payments or watch the webinar, contact us at sales@fire.com. If you would like to be notified about future webinars and updates, feel free to sign up to our mailing list.