Funding the future of cVRPs through the MLA Operator

Article snapshot

As the payments industry prepares for the rollout of commercial Variable Recurring Payments, the creation of a new Multilateral Agreement Operator will be key to ensuring consistent rules and long-term sustainability. By contributing to the initiative, Fire is helping build the foundations for a scalable open banking ecosystem.

How the payments industry is enabling scalable commercial variable recurring payments through a new governance framework.

–

A new phase in open banking payments

The development of commercial variable recurring payments (cVRPs) represents a significant step forward for open banking payments in the UK. Adoption of open banking continues to rise in the UK, with more than 31 million open banking payments made and 1 in 5 consumers and small businesses using open banking in March 2025 alone.

As this momentum builds, recurring payments via bank transfer offer a scalable way to bring recurring payment solutions for businesses into the open banking ecosystem, enabling secure, transparent, and flexible payment experiences for both consumers and businesses.

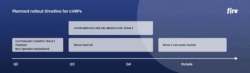

By offering an alternative to card-on-file, direct debit, and standing orders, cVRPs have the potential to offer a compelling recurring payments experience for both consumers and businesses. As the industry prepares for the launch of the ‘pilot phase’, referred to as ‘Wave 1’, targeted for Q3 2025, stakeholders are working to ensure that variable recurring payments solutions are scalable, consistent, and ready for broader adoption.

This article explores the building blocks being put in place to enable commercial variable recurring payments, including the role of Open Banking Limited (OBL), the introduction of a new governance framework, and the industry’s progress toward a sustainable and scalable scheme.

What are commercial VRPs and why do they matter?

While single open banking payments are limited to once-off payments for each authorisation, variable recurring payments (VRPs) allow payers to authorise recurring open banking payments from their current account. “Sweeping” VRPs also known as “me-to-me” payments only allow for payments between the payer’s own current accounts with another account provider, while commercial VRPs (cVRPs) allow third parties such as merchants or billers to initiate multiple payments from a customer’s account under a single consent.

While most major banks in the UK are required to provide APIs for these “sweeping” VRPs, cVRPs for recurring payments between third parties are not mandated, and therefore ASPSPs have had little incentive to provide what is considered “premium APIs” to allow these recurring open banking payments to a third party. This is about to change, with an industry-led initiative underway to define a viable framework including a sustainable commercial model for cVRPs.

The UK’s National Payments Vision emphasises the need to modernise payment infrastructure and regulation to support economic growth. A cornerstone of this vision is the advancement of open banking services, with cVRPs playing a central role. The continued success of open banking will offer both consumers and businesses in the UK enhanced choice, secure payment processing, improved user experiences, and greater efficiency.

Recurring open banking payments will enable merchants to initiate multiple payments within agreed limits, providing a transparent and secure framework for recurring payments. These variable recurring payment solutions expand the range of open banking use cases and have the potential to become a strong alternative to traditional methods like direct debit and card-on-file, especially in sectors such as subscription billing, insurance renewals, utilities, and B2B SaaS, among others.

For customers, cVRPs offer greater security, transparency, and control over payments. For merchants and billers, they bring potential benefits such as reduced transaction costs and improved conversion rates due to a more seamless payment experience.

Wave 1 of the rollout will focus on low-risk use cases defined by Open Banking Limited (OBL), such as payments to utility providers, and regulated financial institutions. Higher-risk use cases, including e-commerce, are expected to follow in future waves.

How collaboration is enabling variable recurring payments solutions

The last year has seen Open Banking Limited (OBL, formerly the Open Banking Implementation Entity), in collaboration with the payments industry, make significant progress in preparation for the anticipated Wave 1 launch later in 2025. This has included drafting a Multilateral Agreement (MLA) – the foundational contract between billers, Payment Initiation Service Providers (PISPs), and Account Servicing Payment Service Providers (ASPSPs) – and work on a sustainable commercial model that will incentivise innovation of this new recurring payment capability.

Recognising the operational complexity involved in scaling the new recurring payment model, the Financial Conduct Authority (FCA) tasked OBL with developing the framework to support their introduction in the UK.

Now in the final stages of preparation, the remaining steps include finalising a commercial model for Wave 1 use cases and establishing the MLA Operator, an independent entity that will oversee the agreement and support the smooth running of the scheme.

The upcoming Wave 1 marks a pivotal moment for open banking in the UK and align with the National Payments Vision’s goals to drive innovation, improve user experience, and broaden access to digital payment methods.

Building the framework: the MLA and its operator

The Multilateral Agreement (MLA) provides the essential governance framework for cVRPs, and the MLA Operator will be responsible for overseeing it.

To support its effective implementation, legally binding agreements and operating guidelines are required. Open Banking Limited (OBL) has drafted and published the MLA, which includes key documents such as the rulebook and participation agreement, and will incorporate the commercial model ahead of the Wave 1 launch.

The FCA and the Payment Systems Regulator (PSR) have tasked OBL with establishing a new, independent entity to oversee the development and operation of the cVRP framework. This independent company will act as the central authority for the scheme. As outlined in the MLA rulebook, the role of the Operator is to “maintain, develop and administer the MLA […] to facilitate the smooth functioning of cVRP”. In other words, this transitional MLA Operator will serve as the temporary governance body responsible for managing the rollout of Wave 1.

Having a clear framework in place is critical to encouraging innovation, ensuring fair and competitive pricing, and establishing clear liability and an effective dispute resolution process. The MLA creates a unified contractual arrangement between the Operator and all participants, offering a level of consistency and operational efficiency that would be difficult to achieve through bilateral agreements.

The industry-led approach to drafting the MLA and setting up the Operator is important as regulatory frameworks are often shaped through a top-down process without consulting key players which can lead to unforeseen issues and unintended consequences. In contrast, engaging stakeholders from across the ecosystem enables a more inclusive, bottom-up model that reflects a broader range of perspectives, supporting the long-term growth of variable recurring payments solutions.

The path to a sustainable scheme

Once the MLA Operator is established and operational, it will oversee the launch of the ‘pilot’ phase of the recurring payment model in the UK, referred to as Wave 1. This phase will focus on low-risk use cases within regulated industries that have been carefully selected for their lower risk profiles. These include utility providers, charities, regulated financial firms and e-money institutions, government bodies, and rail operators.

The ultimate objective is to expand the scheme to cover e-commerce payments, thereby unlocking its full potential. Since these use cases carry a higher risk profile for participants, a sustainable commercial model and appropriate safeguards must be developed.

With this in mind, OBL intends to launch the higher-risk Wave 2 e-commerce use cases at a later stage. While work on the commercial model for Wave 2 will continue in parallel with the launch and rollout of Wave 1, lessons learned from Wave 1 are expected to support a smoother implementation of Wave 2.

Balancing near-term delivery and long-term commercial viability

A recurring challenge in developing a commercial variable recurring payment scheme for the UK has been reconciling the need for long-term sustainability – covering future Wave 2 e-commerce use cases – with the more immediate objective of meeting the Wave 1 launch timeline.

This conflict of priorities is most notable in the development of the commercial model. A key issue raised throughout has been the need to make short-term decisions that support the viability of Wave 1, while also laying the groundwork for a model that will accommodate higher-risk use cases in the future Wave 2 commercial model.

The MLA Operator will ultimately need to assess whether a single commercial model can serve both low-risk and high-risk applications, or whether separate frameworks will be required for the latter. Striking this balance will be vital to the long-term success of commercial variable recurring payments solutions.

Industry funding: enabling collaborative innovation

To support the ongoing developments and foster open banking innovation funding, Open Banking Limited (OBL) has now initiated a new funding round, with 31 organisations participating. These include a broad mix of fintechs, major banks, and other payment providers, reflecting growing fintech investment in VRPs.

This strong level of industry engagement and participation highlights the growing commitment across the payments ecosystem to support the future of commercial variable recurring payments solutions.

Early funders of the work to deliver recurring open banking payments and its operator in the UK have a valuable opportunity to influence delivery and help shape the future of open banking.

Fire’s commitment to open banking innovation

Fire is an active supporter of the development of commercial variable recurring payments in the UK. We are committed to industry collaboration and innovation, and our team contributes to working groups focused on progressing open banking developments in the UK and Ireland.

Our investment in this initiative reflects Fire’s core values: driving innovation internally, understanding market needs, and supporting broader industry progress. We see this as a pivotal step in the evolution of open banking.

We believe in the importance of industry-led initiatives and value the opportunity to bring our perspective to the table. This helps ensure that innovation remains aligned with customer needs and, in future, enables the delivery of commercial variable recurring payments solutions that offer real value.

What’s next for commercial VRPs?

2025 is set to be a pivotal year for the rollout of cVRPs in the UK, which as mentioned should see the rollout of recurring open banking payments in low-risk, regulated industries such as charities and utilities providers. The current plan is to finalise the commercial model and establish the MLA Operator to enable the launch of Wave 1, focused on low-risk use cases.

Work on Wave 2 use cases – such as e-commerce, which carry higher risk profiles – will continue in parallel. These use cases require further consideration, including potential modifications to the framework or the introduction of alternative commercial models to ensure resilience.

Insights from the rollout of Wave 1 will play a crucial role in informing the development and refinement of the framework for Wave 2. This staged approach ensures that lessons learned from initial implementations can be applied to facilitate the successful launch and broader adoption of higher-risk e-commerce use cases in future phases.

The path forward for open banking payments

In summary, cVRPs which allow recurring payments to retailers with a once-off customer authorisation, hold strategic importance for the future of payments, with the MLA Operator, funded by organisations across the open banking and payments industries, playing a central role in enabling their scalable development. Ultimately, they have the potential to redefine the recurring payments landscape across both B2C and B2B sectors, delivering greater efficiency, stronger security, and an improved user experience.

Sustained industry-wide collaboration will be key to the successful implementation and long-term impact of commercial variable recurring payments solutions.

We welcome any thoughts you may have on the development of commercial Variable Recurring Payments. If you have questions or would like to discuss this topic further, please reach out to our team. Our experts are available to provide insights and assistance.

Article snapshot

As the payments industry prepares for the rollout of commercial Variable Recurring Payments, the creation of a new Multilateral Agreement Operator will be key to ensuring consistent rules and long-term sustainability. By contributing to the initiative, Fire is helping build the foundations for a scalable open banking ecosystem.