Getting a new Business Account shouldn’t be a “big move”.

Opening a new business account shouldn’t be a big move. With Ulster Bank now sending out thousands of letters to businesses across Ireland, customers will be assessing their options and deciding what works best for them. We at Fire are here to help business customers of Ulster Bank.

We aim to make a Fire business account an ideal alternative for Ulster Bank Business Customers. Businesses may apply online, so no branch visits or delays, the accounts are low cost and include a great range of payment services to cater for all business needs.

Who we are

Fire is an Irish headquartered business, founded in 2010 by Colm Lyon, one of Ireland’s leading fintech and payments entrepreneurs. The business is regulated by the Central Bank of Ireland as a payments institution since its establishment. The team is based in the CHQ Building on the North Quays in Dublin. We also have offices in London, UK where we have been regulated by the FCA since 2019 (post Brexit).

Fire has thousands of business customers across Ireland and the UK including some very large financial institutions. As an Irish business we aim to understand the needs of the local market.

What’s a Fire Account

With a Fire Business Account you will get access to:

euro and sterling accounts – open as many as required

all the debit cards you need for your business and staff

bank transfers, FX services, pay by direct debit

mobile app for real time notifications and security

open banking payments – so you can get paid more easily

integration options for accounting systems

Additionally with a Fire Business Account, customers can integrate their systems for better reconciliation and straight through automated payment processing.

As Fire is a local and regulated account provider, all euro accounts have Irish (IE) IBANs, and sterling accounts have UK sort code/ account number – so former Ulster Bank business customers will have no problems paying and getting paid.

How to apply

Our mission is to remove friction and hassle for businesses when it comes to accounts, cards and payments. You can apply for an account here and the process is completely online – so no branch visits and no waiting lists to see someone to talk about opening an account. You’re in control.

Apply below or reach out to our sales team for more information at sales@fire.com

We are delighted to release improvements to the Fire Open Payments User Interface to all customers. At a high level, Open Banking and our payment requests enable businesses to accept account-based payments from their customers.

The most exciting change is that you can now customise the design of the Fire Open Payments pages! In this new update, you can add your business logo, edit the page colouring, and even include additional text fields. If you are interested in making some minor changes to the Open Payments pages, please let us know by mailing support@fire.com and we can schedule a meeting to work through some of your requirements.

We have a couple of other functional changes to the Open Payments flow, but the majority of changes are in relation to the User Interface only. In updating the flow, we have sought to shorten the customer journey and make it more appealing and intuitive across the desktop and mobile interfaces.

Mobile Flow

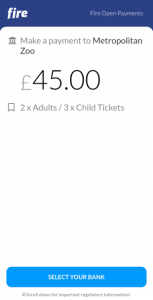

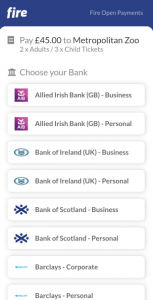

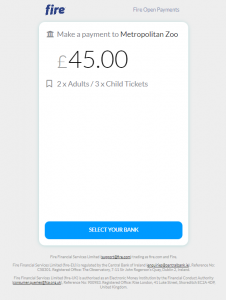

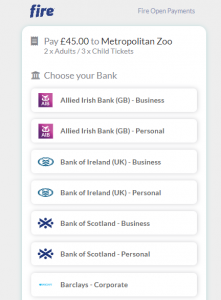

1. Payment Details Page

The Payment Details Page is the first landing page for customers on the Fire Open Payments journey. They can be redirected here from a merchant’s shopping cart, or scanning a QR Code, for example.

Within the new flow, the user can see both Payment Details and select their ASPSP on the same step, shortening the journey by one page.

Functional Improvements:

The URL of the old second page https://payments.fire.com/{code}/aspsps has now been removed.

The URL of the new first page is still https://payments.fire.com/{code}, but the user will now go directly to the consent page https://payments.fire.com/{code}/aspsps/{aspspUuid}.

If you are routing your customer directly to https://payments.fire.com/{code}/aspsps, you will need to change this to https://payments.fire.com/{code} or https://payments.fire.com/{code}/aspsps/{aspspUuid}.

The addition of a Cancel and Return button. This will return the user to your returnUrl (if specified – otherwise the button will not be visible) with the following URL: {yourWebsite}/return?status=cancelled. You can use this to return the customer to their shopping cart.

This button will be visible up until the user consents to a payment.

Current Pages

New Page

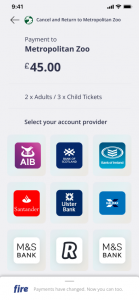

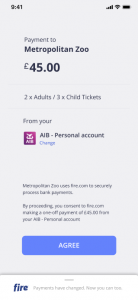

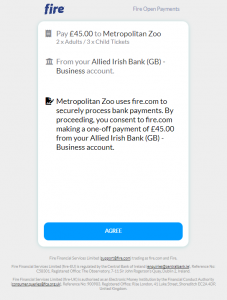

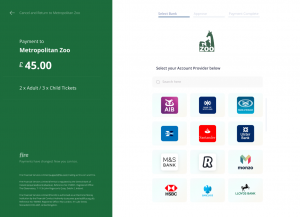

2. Consent Page

The Consent Page contains regulatory text Fire are required to display. At this point, when the customer clicks the ‘AGREE’ button they will be redirected to their third-party ASPSP/bank to authorise the payment.

Current Page

New Page

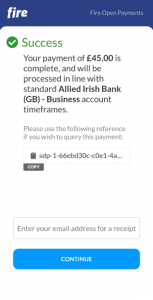

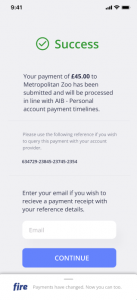

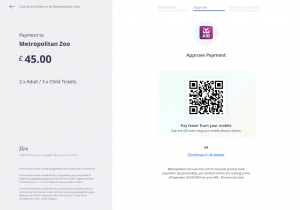

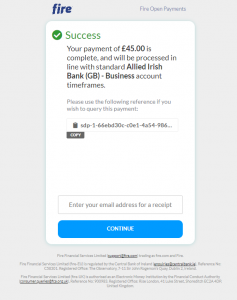

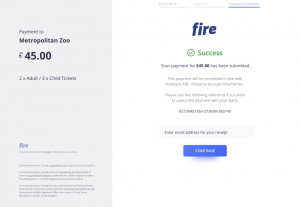

3. Response Page

Once the user authorises the payment via their third party ASPSP/bank, they will return to the response page. On this page, Fire displays the status of the payment to the user, as well as a reference they can use to query the payment.

Current Page

New Page

Desktop Flow

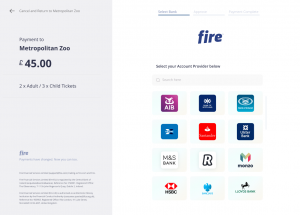

1. Payment Details Page

The Payment Details Page is the first landing page for customers on the Fire Open Payments journey. They can be redirected here from a merchant’s shopping cart, or scanning a QR Code, for example.

Within the new flow, the user can see both Payment Details and select their ASPSP on the same step, shortening the journey by one page.

Functional Improvements:

The URL of the old second page https://payments.fire.com/{code}/aspsps has now been removed.

The URL of the new first page is still https://payments.fire.com/{code}, but the user will now go directly to the consent page https://payments.fire.com/{code}/aspsps/{aspspUuid}.

If you are routing your customer directly to /aspsps, you will need to change this to /{code} or /{code}/aspsps/{aspspUuid} if you host the list of banks on your website.

The addition of a Cancel and Return button. This will return the user to your returnUrl (if specified – otherwise the button will not be visible) with the following URL: {yourWebsite}/return?status=cancelled. You can use this to return the customer to their shopping cart.

This button will be visible up until the user consents to a payment.

Current Pages

New Page

2. Consent Page

The Consent Page contains regulatory text Fire are required to display. At this point, when the customer clicks the ‘AGREE’ button they will be redirected to their third-party ASPSP/bank to authorise the payment.

Current Page

New Page

3. Response Page

Once the user authorises the payment via their third party ASPSP/bank, they will return to the response page. On this page, Fire displays the status of the payment to the user, as well as a reference they can use to query the payment.

Current Page

New Page

Customisation Example

As alluded to in the introduction, Fire is excited to offer our customers the capability to put your own stamp on the payment pages.

You can customise anything from the background and text colours, to the text displayed within action buttons and adding your own business logo.

Please feel free to reach out to support@fire.com if you are interested in working on customised options.

Default User Interface

Customised User Interface (example)

Conclusion

We are excited to be launching these changes to our Open Banking and we hope they streamline the experience for you and your customers.

For more detailed information and troubleshooting, be sure to check our Business Banking FAQs, designed to assist with a smooth transition to the new system.

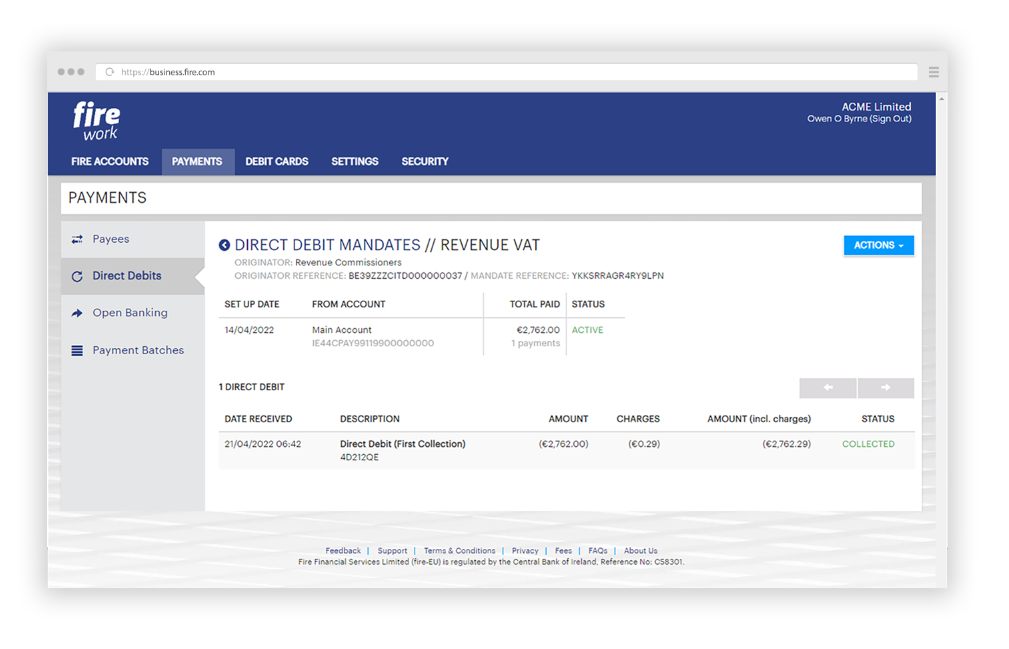

We are pleased to announce that our business and personal customers may now pay by direct debit from Fire euro accounts. Direct debit is a very common way to pay for utility bills, card acquirer charges, Revenue Commissioners taxes and other regular payments, with the funds taken directly from your account automatically at a specified date. Direct debit payments have been available on Fire sterling accounts for some time, so with the addition of this new feature we hope that more customers will use Fire for more of their day to day payments.

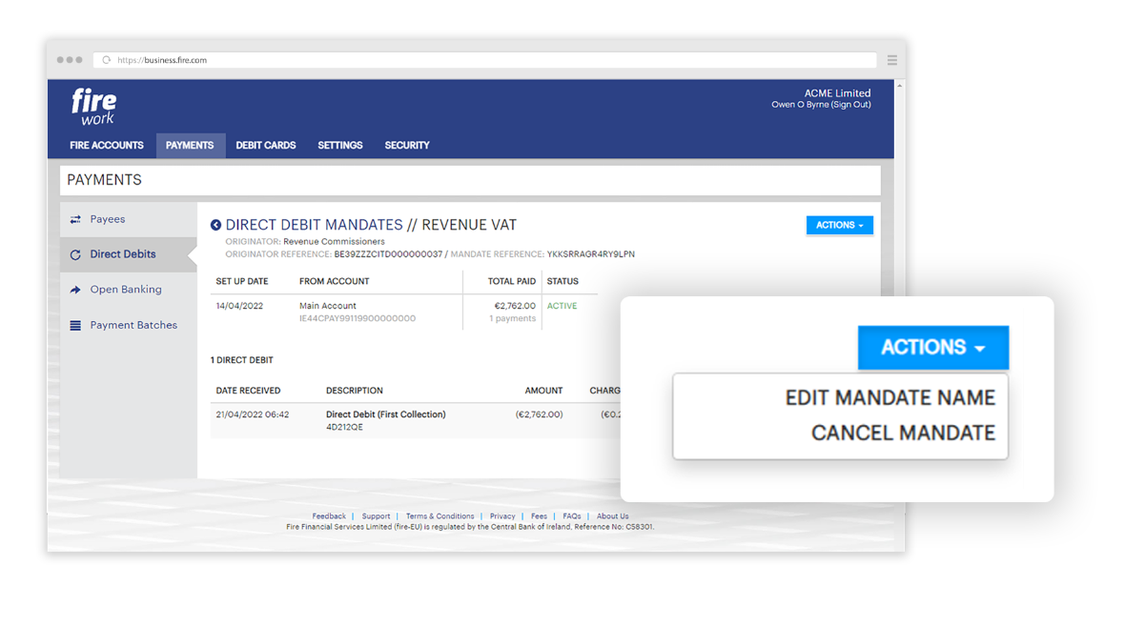

All of your direct debit mandates – the permission you give billers to take funds from your account – are available to see and manage using the Fire online portal.

Managing direct debit payments with Fire

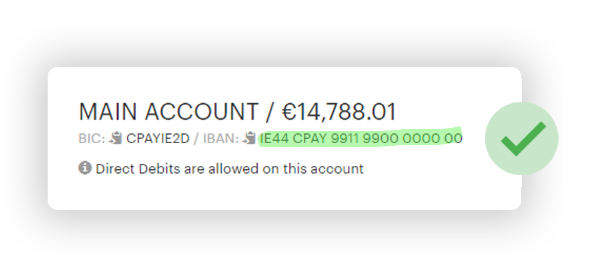

For a euro direct debit to be collected from your account, you will need to provide the direct debit collector with your account name, and your Fire IBAN.

IE IBANS – all your euro Fire account are issued with “IE” IBANs so there should be no issue with businesses collecting funds from your Fire accounts.

Disable DD collections – your euro Fire accounts are by default enabled for direct debit payments. You may disable the collection of direct debits for each account using the “Actions” menu.

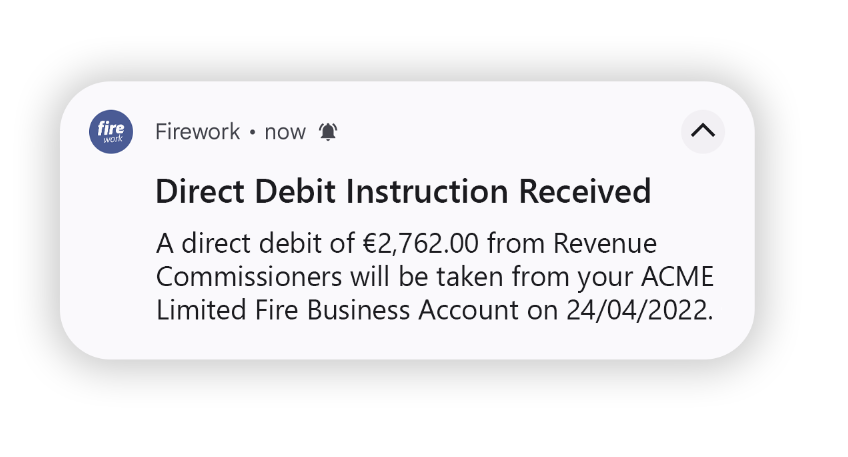

Notifications – you will receive notifications in advance of any direct debit payments due from your account.

This gives you time to ensure you have the funds to cover the payment, and helps with cash flow planning. If you feel you shouldn’t be paying a certain direct debit, you can cancel the mandate easily to prevent funds being taken from your account (but be sure to let the biller know so they can correct the issue).

Fire already supports payment by direct debit from sterling accounts, so now, with Fire, you can pay by direct debit in both currencies. This new feature is available to all personal and business customers.

Fire provides euro and sterling accounts, debit cards, and a range of payment and integration services – check out our full features page for more information.

This new feature is particularly advantageous for both business and personal account holders, simplifying the management of regular payments and enhancing financial control.

We look forward to introducing more features to the Fire business account throughout 2022. If you have any feedback or queries on this feature release, please do get in touch by emailing support@fire.com.

For more information and answers to any questions you might have about this new feature, or any other aspect of your Fire account, be sure to visit our Business Banking FAQs. You may also want to check out our page on frequently asked questions about personal accounts. This resource provides comprehensive and helpful information to make managing your finances with Fire a smooth and efficient experience.

In a previous blog post we described the payouts pain point some businesses experience today, how Fire can help automate this process and examples of automated payout processes some Fire customers have implemented today. In this blog post we’ll walk you through the steps needed to set up an automated payouts process in your organisation using payment batches via the Fire API.

Application Set-Up

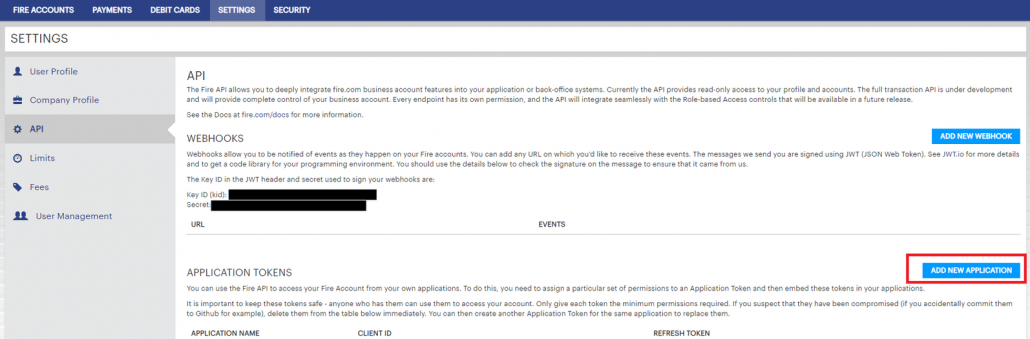

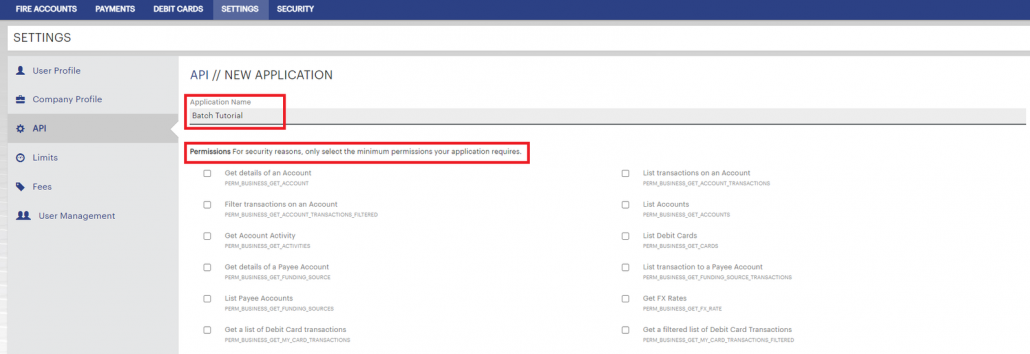

Firstly, you will need to set up set up a Fire Application to access the Fire API. To do this:

Give you API Application a name, and select the required permissions.

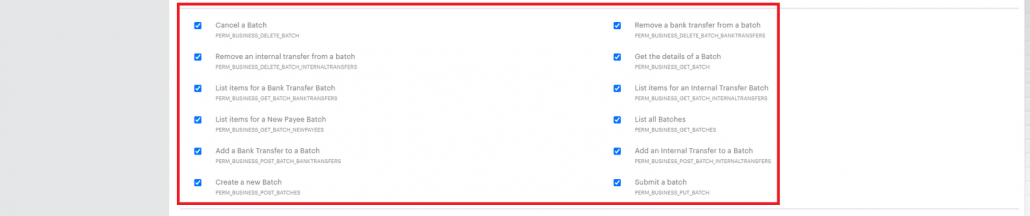

For this Tutorial we will be showcasing the Batch functionality so select the Batch permissions below:

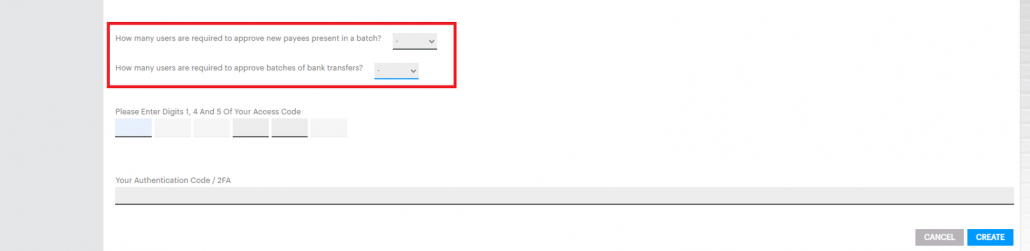

You then can configure how many approvers are need prior to processing a batch. There are 2 types of approvals:

Approvals for adding a new payee for a batch – in line with legislation, you are required to approve new payees on your account using Strong Customer Authentication (SCA). The first time you make a payment to a payee, Fire will send notifications to Full Users so they can approve. This will be a single notification containing the details of all the new payees in the batch. Once a payee has been approved on your account, it is not necessary to approve payments going forward (although you can can opt to approve all payments – see below).

Approvals for batches of bank transfers – you can set this to 0 to automatically process batch payments to previously approved payees. This is useful for setting up unattended automated batch payments.

You can also have multiple approvers if you want for either type to enhance security. All full users will get a push notification to approve to their linked mobile devices to approve the batch.

Once you’ve finished above, click “Create“, and take note of your Client ID, Client Key and Refresh Token – the Client Key will not be displayed again.

Note If you ever accidentally reveal the Client Key (or accidentally commit it to Github for instance) it is vital that you log into firework online and delete/recreate the App Tokens as soon as possible. Anyone who has these three pieces of data can access the API to view your data and set up payments from your account (depending on the scope of the tokens).

Authentication

You now use these pieces of data to retrieve a short-term Access Token which you can use to access the API. This will be set as the Bearer Token in the ‘Authorization’ header for all API calls. For security reasons, the Access Token expires within a relatively short timeframe – there is a 15 minute window to use it.

In order to create an Access Token, you require:

Client ID – The app’s Client ID created above.

Refresh Token – The app’s Refresh Token created above.

Nonce – A random non-repeating number (that is incremented from the previously used value) used as a salt for the clientSecret below. The simplest nonce is a unix time.

Client Secret – A Client Secret is the a SHA256 sum of the nonce concatenated with the Client Key: sha256(<NONCE><CLIENT_KEY>)

To retrieve the Access Token, send a POST request to https://api.fire.com/business/v1/apps/accesstokens containing the following JSON body:

You will receive an Access Token and details of the allowed permissions in response:

Once you have the access token, pass it as a header for every API call, like so:

Authorization: Bearer $ACCESS_TOKEN

Whenever it expires, create a new nonce and get a new access token again.

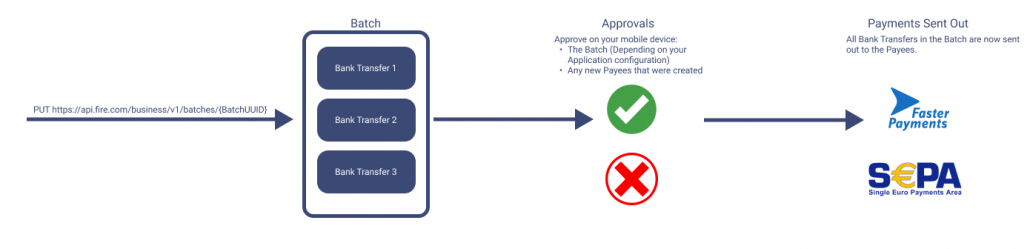

Processing a Batch

The process is as follows:

Create a new batch

Add payments to the batch

Submit the batch for approval

Download a Postman Collection which contains all of the main batch calls you can use to follow along with this tutorial.

In Postman, you can import this collection by copying this URL and pasting it in the import section.

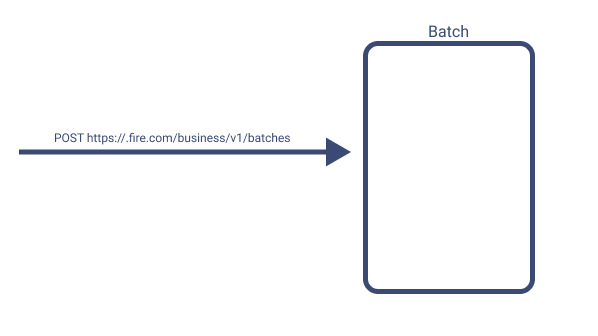

1. Create a new Batch

The first step in making a making a batch payment is creating the batch itself. The batch object can be thought of as a container which you can add multiple payments to which are to be made at the same time. The batch object specifies the name, currency and type of the batch.

There are 2 batch types you can create:

INTERNAL_TRANSFER – All the payments are funds movements between your own Fire accounts.

BANK_TRANSFER – All the payments relate to fund movements outside of your own Fire accounts (e.g to a Payee)

For this tutorial, we will be making a BANK_TRANSFER batch. Send a POST request to https://api.fire.com/business/v1/batches with the following JSON:

callBackUrl:An optional POST URL that all events for this batch will be sent to – see the section on webhooks below.

batchName: An optional name you give to the batch at creation time. Say January 2018 Payroll.

jobNumber:An optional job number you can give to the batch to help link it to your own system.

You will receive the batch UUID in response:

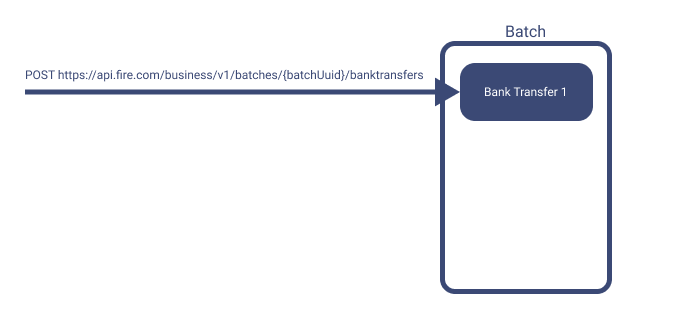

2. Add a bank transfer to a Batch

Now that we have a batch UUID, the next step is to add some bank transfers to the batch. This is done by passing the account details, amount and references to the API. If the account details relate to an existing payee, the batch will be processed as normal. If this is your first time making a bank transfer to these account details, you will get a push notification to your phone to approve the new payees in the batch once you submit the batch in the next step. Once these new payees have been approved you won’t need to approve them again in future batches.

POST the bank transfer details as a JSON object to https://api.fire.com/business/v1/batches/{batchUuid}/banktransfers

You will receive a bank transfer item UUID in response. You can use this UUID to query the status of the payment, or to remove the payment from the batch.

3. Submit the batch for approval

Once you have added all the bank transfers you wish to make, it is now time to submit the batch to make the payments. Send a PUT request to https://api.fire.com/business/v1/batches/{BatchUUID}. This will result in a 204 NO CONTENT response.

Depending on how you configured the API keys above, this may trigger a request for approval to all full users of the account. They can login to the Firework mobile app to view the details of the requests and approve/reject. Once approved, all the bank transfers in the batch are sent out to the payees and the batch process is complete.

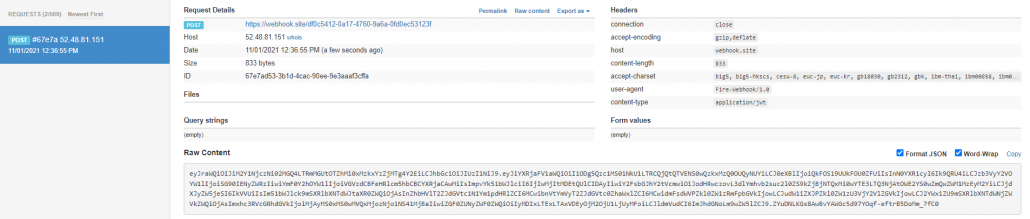

Callback/Webhook real-time notifications:

If a callbackURL was specified in the Create Batch API call, you will be notified in real time when payments are submitted, approved and complete. This is a popular feature Fire offers and will allow your systems to make real time updates accordingly.

Below is an image (using webhook.site) to showcase what a webhook call may look like:

Each webhook call will contain a JWT payload (as seen in the Raw Content section) in the body. You can decode this JWT payload token to JSON in your own code, or by going to https://jwt.io for testing purposes. Your system can now receive live updates when Batches are made, approved or submitted.

Jake McCarthy is a Product Analyst at Fire with experience across partner payment solutions, transaction monitoring and payment processing.

Open Banking Payments provide a disruptive alternative to online payments, but what does an actual payments journey look like for a customer? If you have been following the fire.com blog over the last number of weeks, you may have noticed that we have quite a number of Open Banking Payments initiatives, from the Irish Guide Dogs Day through to our own Open Banking Terminal. These are exciting developments, both for us as a company or enterpise, but also within the larger Open Banking sphere. However, quite understandably, the concept of Open Banking and Fire Open Payments is still an unknown to the vast majority. That is the inspiration for this blog post – to shed some light around the Fire Open Payments journey and, hopefully, prompt more of you readers to consider trialling the process yourselves!

The Open Banking journey with Fire Open Payments

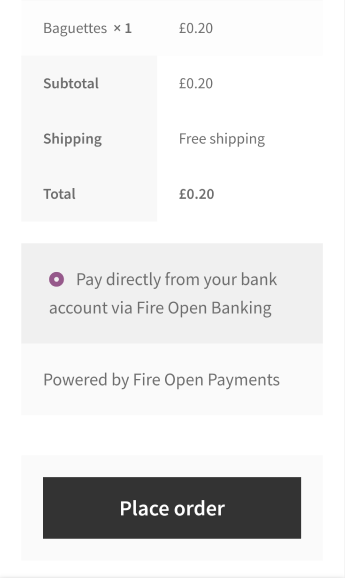

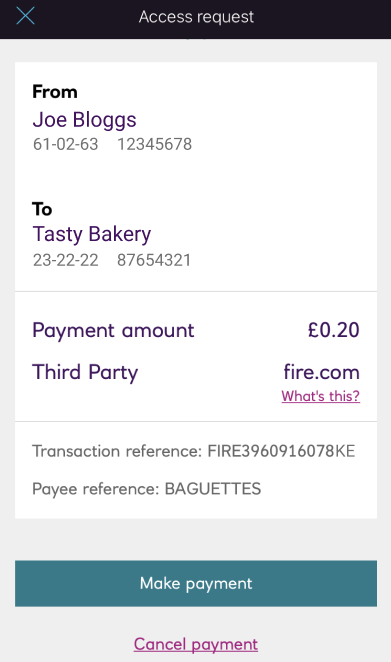

For this particular journey, I am on an e-commerce website and want to purchase a baguette from my local bakery – Tasty Bakery.

Similar to any e-commerce flow I select my products, and go to the “Checkout”. After entering my Delivery Details I then proceed to payment. At this point most of us would be used to fumbling around for our purse/wallet, then squinting to transcribe the card number into the website.

However, with just a tap of a button, I am redirected to the Fire Open Payments journey.

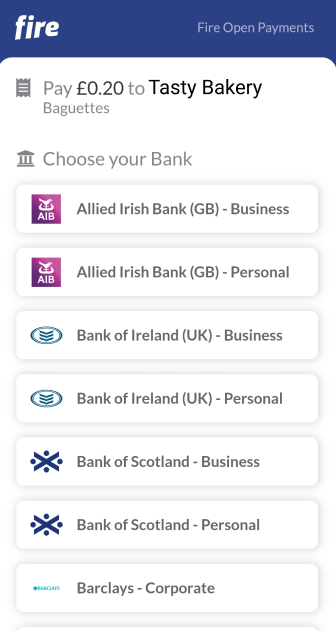

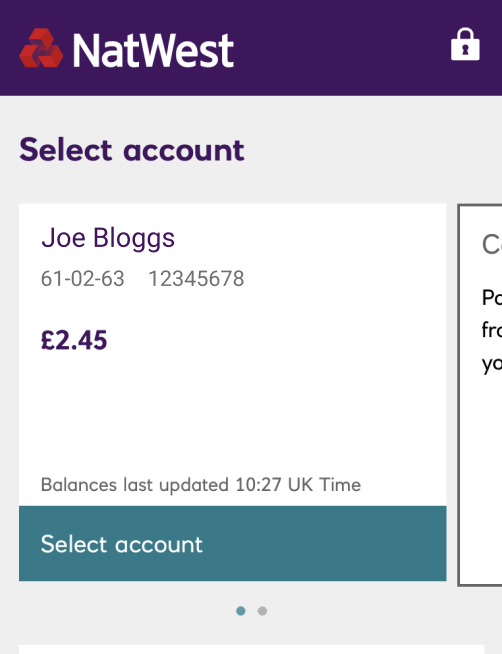

I select my bank of choice from the list.

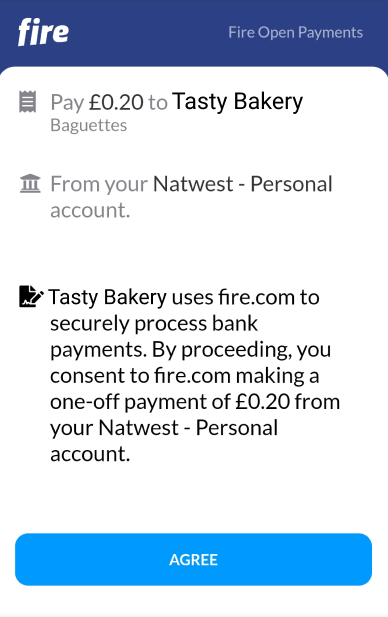

I bank with Natwest, so I’ll select them from the list. I then consent to the payment, which will redirect me to my Natwest banking app.

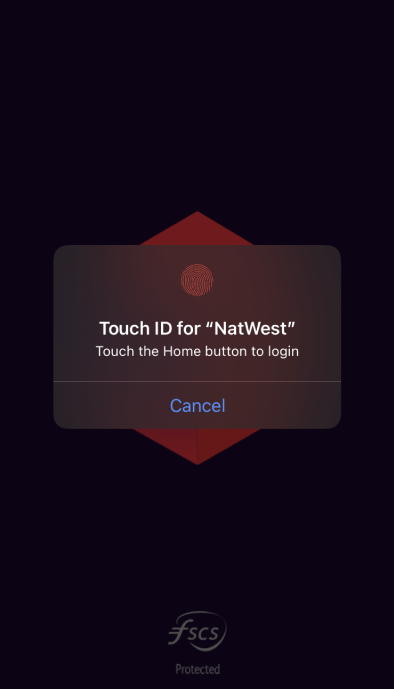

I will be prompted to log in to my Natwest app to authorise the payment. This part of the journey will be dictated by the bank itself in terms of how it designs their app flow.

This is an important part of the journey; it ensures that the customer who initiated the payment is the account owner and not attempting to make a payment fraudulently.

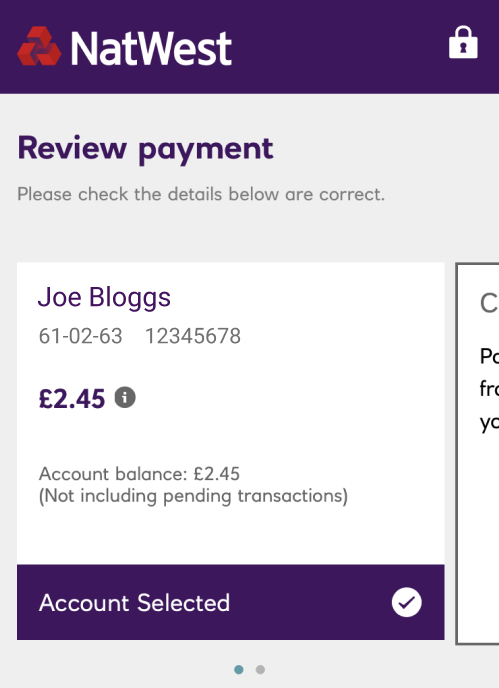

After scanning my fingerprint, I select the account I wish to pay from.

A quick tap of the ‘Account Selected’ button and I can authorise the payment.

Thankfully my account balance just stretches to cover the payment and I will be able to complete the purchase!

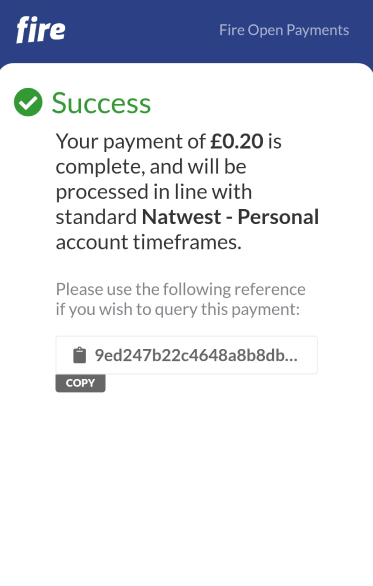

I will then be returned to my browser where I see that the payment has indeed been successful. I can request an optional receipt before returning to the merchant website, where I will hopefully be informed that my baguette will be delivered fresh from the oven.

Conclusion

There you have it, I’ve managed to make a payment through Fire Open Payments. The main benefits to my mind is the flow itself and the enhanced security. I never had to divert my attention from my phone to complete the payment; everything is contained within my browser and banking app. Having the flexibility to choose the account to pay from, coupled with a live view of my account balance was a bonus too.

This process provided that added assurance by authenticating the payment using my fingerprint – I was confident that no one could fraudulently create a payment on my behalf without access to my thumb! Also, if you’re security-conscious like me, I never save my card details within the browser, so I regularly find myself leaving the comfort of my couch to retrieve my debit card to enter my card number. This step was completely bypassed through Open Banking.

If you are curious about trying the process yourself, scan the QR code below or head over to https://www.fire.com/donate to make a small donation to Calcutta Connect and trial the Open Banking experience.

The way in which merchants accept payments and the devices/terminals used to facilitate these transactions have undergone quite the evolution over the past 70 years. Merchant acquiring technology now comes in many form factors tailored to the business needs of each merchant case. Although, over this time cards have remained the primary payment method which consumers rely on. The introduction of open banking payments unlocks the potential for a new paradigm shift away from cards and towards account based payments. Merchants are beginning to realise the benefits that come with this new payment mechanism and consumers are becoming familiar with a new payment flow.

In this blog post we’ll:

Cover a brief background on the evolution of merchant devices and consumer payment methods.

An overview of open banking payments and the benefits they can provide to merchants.

Introduce the Open Banking Terminal by Fire – transforming your mobile device into a point of sale terminal ready to accept open banking payments straight into your Fire Business Account.

A Brief History of In-Person Payments

When looking back at the evolution of in-person payments we’re going to be focus specifically on the consumer payment method – how are funds exchanged between the merchant and consumer and how quickly does the merchant receive the funds?

Evolution of consumer payment methods over time

The primary consumer payment method by and large remained unchanged until the first big shift from cash to card payments with the introduction of the Diner’s Club charge card in 1950. Since then, we’ve seen card technology go through many iterations from the conception of the card networks in the 1950’s, the introduction of the magnetic strip in the 1980’s, EMV technology in the 1990’s and mobile wallets in 2008. All leading to more secure and accessible card payments. Although incremental improvements were made over that time the primary consumer payment method largely remained the same, a card payment. The same financial players are involved: issuers, merchant acquirers, card networks and numerous intermediary service providers. Open banking payments help facilitate the next big shift in consumer payment methods from card to account-based payments.

Open Banking Payments and its Benefits to Merchants

As covered in our previous blog post, “Open Banking Payments – What needs to happen next?”, open banking payments in the EU and UK can be traced back to the introduction of the second Payment Services Directive (PSD2) and it’s associated regulatory technical standards (RTS).

With these account based payments there are a number of benefits for merchants and consumers alike:

Cost-Effective – No hardware required. Accepting payments through the Open Banking Terminal is cheaper than other ways to get paid. No monthly or recurring fees, just one low transaction fee and reduced chargebacks.

Quicker Settlement – By executing payments via Faster Payments (Sterling) or SEPA (Euro), funds settle into your Fire Business Account quickly – within 6 business hours. Reconciliation is automated.

Less Fraud – The Open Banking Terminal is one of the safest ways to collect payments. No personal credentials are needed, reducing the risk of fraud.

The Open Banking Terminal by Fire

With the introduction of the Open Banking Terminal by Fire, merchants can realise the benefits of the shift towards account based payments from within the Fire Business Mobile App. Allowing any merchant to quickly accept ad-hoc payments from their customers on the go and have collect the funds straight into their Fire Business Account within 6 business hours.

Enter the amount to be paid in the Fire Business Mobile App.

A QR code is generated in the app to be presented to the customer to scan.

The customer scans the QR code and picks their bank.

The customer consents to the payment.

The customer are redirected to their Bank’s mobile app.

The customer reviews and authorises the payment from within their Bank’s mobile app.

The customer and the business receive confirmation that the payment was authorised and will be processed.

Check out our announcement video to see the full Fire Open Payments Terminal flow in action here.

fire.com is one of the UK and Ireland’s major Open Banking providers. To get your hands on the Open Banking Terminal by Fire and start accepting Open Banking Payments today, set up a free business account and download the Fire Business Mobile App today.

Jake McCarthy is a Product Analyst at Fire with experience across partner payment solutions, transaction monitoring and payment processing.

Open Banking was, at one time, set to give consumers access to their bank and e-money accounts with the ability to share information and initiate payments via regulated third party providers. It was a great ambition to bring competition, innovation and a new set of players into the market. It was envisaged that fintechs would bring new benefits to businesses and consumers, allowing secure ways of sharing information and making online payments. It would herald the end of screen scraping and move the industry to API based integration. There are countless benefits that these changes would bring.

A few years on, we find ourselves at a crunch point – a critical time for the era of open banking.

How it started

As a digital account provider, Fire are particularly interested in the payments aspect of open banking. In fact, our interest in open banking payments stems back over ten years. Fire was initially a part of a card based payment gateway business for online retailers called Realex Payments. Back then we set up Fire to be the “collections” account for retailers who wished to get paid when accepting payments directly from their customers’ accounts, rather than accepting cards. Account-based payments remain a major payment method in various countries across Europe.

The arrival of the second Payment Services Directive (PSD2) and its associated Regulatory Technical Standards (RTS) created the legal and regulatory environment for new account information (AISP) and payment initiation service providers (PISP). We became regulated for both account information and payment initiation services, knowing that account-based payments worked extremely effectively in other regions. We also could see that account-based payments were a preferable option for certain retailers to be paid by consumers.

Account based payments offer huge benefits for both retailers and consumers. These benefits include better security, less sharing of sensitive data, lower fraud, potentially lower processing costs and faster settlement times for payees (retailers). Driven by our experience and seeing the underlying value proposition, we set about building Fire Open Payments, an open banking payments solution for retailers to accept payments directly from their customer’s accounts.

How it’s going

In terms of how open banking payments are progressing, it’s a very different story in the UK and the EU. Fire operate and are regulated in the UK and the EU. At a recent UK Open Banking event, a speaker noted that there were as many TPPs active in the UK as there were in the whole of Europe.

The UK has become the undisputed leader in Open Banking. The creation of the Open Banking Implementation Entity, via the CMA, has led to the development of a coordinated approach by the nine largest UK account providers (ASPSPs). This gave rise to the creation of the first era of open banking in the UK. While It is by no means complete, the fundamental building blocks are solid. In addition, the ecosystem remains open and engaged. All stakeholders – from consumer groups, regulators, trade associations, account providers and TPPs are participating in healthy discussions about how best to shape the future. The possibilities for open banking payments remain very strong in such an ecosystem with numerous issues on the agenda, all of which are monitored by regulatory eyes.

In the EU and specifically in Ireland, where Fire is based, the adoption of open banking payments is at the other end of the spectrum. Open banking has not yet taken off. So what’s gone wrong?

To make open banking payments a reality, the ecosystem needs to see a standard implemented in a consistent way. This ecosystem should encourage account providers and third parties to interact and attempt to implement a customer experience that is not just compliant, but a frictionless experience. The UK outcome has clearly demonstrated that this is possible. The fact that the Irish market has not achieved the same level of success as the UK has nothing to do with regulation. The delay in implementing an acceptable user experience by some Irish account providers, when their customers are accessing their account via third parties, has had a serious and detrimental effect on Ireland’s open banking ecosystem. This has been a major barrier for fintechs to bring new benefits to businesses, consumers and the economy at large. The fact the the UK based customers of these institutions enjoy a better experience confirms that the capability exists and leaves us all to wonder why this situation has evolved. Meanwhile, Irish businesses and consumers are being denied the benefits of open banking payments. To put the situation into context, we had a client who was accepting open banking donations that had a conversion rate of 4% with one Irish bank.

What to do next

In terms of what should happen next, we see the UK and Irish markets with a different set of priorities.

In the UK there is recognition of the excellent work completed to date, along with a sense of reality that we are still at the early stages in the development of open banking payments. With the CMA order coming to a rightful close, a transition period will need to be managed as a new entity emerges to carry on the work of the OBIE. This process is currently underway. In addition, specifically in relation to payments, we see this as an opportune time to identify and discuss any barriers and accelerators that could fuel the adoption of open banking payments. Issues such as fragmentation of the market, API uptime, implementing a decoupled experience, devising limits for open banking payments akin to contactless payments, enhancing the exchange of data at payment initiation time to assist with fraud and how variable repeat payments could be rolled out to the full ecosystem and apply to more use cases. These are great topics to be discussing as they all build on what is already in place. We believe the other aspect of open banking payments in the UK that needs consideration is the status of the payment pillar within the new entity. The concept of this being a “Payment Arrangement” is worth examining as it could help to ensure that there is a governance and operating model that is inclusive of all players. This would mean that open banking would have the appropriate level of regulatory oversight.

For the Irish market, there are different actions that we would suggest. Given that the market is behind in its development, we believe that some policy oversight is required. As things stand, TPPs have no indication as to when the issues will be addressed, rendering market and sales planning a fruitless exercise. Leaving the market to sort itself out will delay the delivery of a vibrant open banking ecosystem and continue to deny businesses and consumers the benefits of cheaper, faster and safer payments. Unlike the UK, the Competition and Consumer Protection Commission (CCPC) in Ireland has not issued any remedies to address the issues. However, such action may not be necessary if the CCPC, the Central Bank of Ireland (CBI) and the Department of Finance were to coordinate a forum and express their clear expectations with respect to the development of open banking payments in Ireland. Such an action would be the first step and could potentially be sufficient to address the issues. The problem is, who will take the first step?

From 1st April 2020, fire.com Mastercard® debit card holders can now make contactless card payments of up to €50.00 / £45.00. This change is part of an industry-wide movement to help prevent the spread of Covid-19 by reducing the need to enter PIN codes on card terminals or handle cash.

The increase from €/£ 30.00 is being implemented across the payments sector with the hope that minimising the handling of cash and reducing physical contact with payment terminals and cash registers, as well as cutting queue times when purchasing goods, will have a positive impact on our collective wellbeing.

In order to use the feature, the software on card payment machines must also be updated to accept the new limits. This is occurring gradually across the retail sector. Grocery stores that have successfully rolled out the update include Asda and Iceland.

The contactless limit was increased for all fire.com debit card holders on Wednesday 1st April with no disruption to services. fire.com will ensure it responds appropriately to Covid-19 and take any actions that help protect our customers. For further updates please visit our dedicated COVID-19 page.

For detailed insights and common inquiries related to this update and other aspects of your personal account, you might find our Personal Account FAQs page helpful.

If you’re thinking of setting up your own e-commerce business, online marketplaces can be a good way of reaching a wide audience at a comparatively low cost, leveraging market trust and gaining access to tried and tested commercial models.

One of the more popular online marketplaces is Amazon. Through its Amazon Marketplace network, vendors can access over 2.5 billion monthly customers and 24 years of lessons learned.

There are three main ways you can use Amazon Marketplace to set up and run your business:

Selling on Amazon

Fulfilment by Amazon (FBA)

Merchant Fulfilled Prime

Selling on Amazon is a no-commitment plan that gives you access to all of Amazon’s clientele, your own hosted page and the ability to sell directly into most of Europe.

With FBA, you leverage Amazon’s operations to store, ship, stock and fulfil orders. As the seller, your responsibility is to send stock to Amazon’s warehouse, and, from there, Amazon will take care of the rest of the supply chain – including processing returns and customer support. FBA comes with added benefits such as the opportunity to feature at the top of a search page and having your product pages stamped with the trusted ‘Fulfilled By Amazon’ badge.

The final model is Merchant Fulfilled Prime, which is where the seller uses Amazon’s Prime features and benefits only, taking care of stock and fulfilment in-house.

There are many resources that can support you to get started selling on Amazon. A good source is Marketplace Superheroes. Their programme walks you through how to start and grow a global business on Amazon from scratch. The course not only teaches you how to sell, but what to sell – as well as providing support from experienced Amazon sellers.

Once your business is set up on Amazon, you may want to think about opening a business current account to make it easier to keep track of spending.

Many online Amazon merchants find the fire.com business account a good fit, as compared to traditional current accounts it’s quicker, and simpler, to open. Once the team has approved your online application your new digital account should be live and ready for use within 48 hours.

Other suitable features include:

Dual currency euro and sterling account – When opening a fire.com business account you are automatically given a euro and a sterling account. The sterling account has its own sort code and account number, while the euro account has an Irish IBAN. This means that payments received from EU Marketplaces can be routed to your fire.com euro account, while products sold on Amazon’s UK website can be paid into your fire.com sterling account, avoiding extra FX charges.

24/7 access and control – With the firework mobile app and web portal, users can access their account anytime, anywhere. All of the fire.com business account features are self-service. You can easily make changes, such as opening another account, in euro or sterling, at the touch of a button. It’s ideal for e-commerce sellers who need a fully digital, on-demand payment solution to complement their web-based business.

Full visibility – Event-driven notifications alert fire.com account users to activity within their accounts in real-time. With a fire.com account you can gain peace of mind knowing when you’ve been paid and that actions have been completed successfully. For many Amazon Marketplace sellers, their online business is an additional revenue stream and not their full-time job. Knowing that payments are being made without having to sign-in is an ideal feature for time-strapped merchants trying to balance their marketplace business with other priorities.

Taking the plunge into entrepreneurship and setting up your own marketplace business can feel daunting, but there are many resources you can tap to ensure you get off to the best start possible. It’s always useful to start by finding an existing group or network that has been on the same journey as you and leveraging shared knowledge. Once you are armed with lessons learned, think about priming your business for growth by ensuring all of your processes are built to scale. This can be achieved on the payments side by opting for an account provider that has invested in features that look to simplify incoming and outgoing payments and make it easier to get paid across borders.