Open Banking Payments provide a disruptive alternative to online payments, but what does an actual payments journey look like for a customer? If you have been following the fire.com blog over the last number of weeks, you may have noticed that we have quite a number of Open Banking Payments initiatives, from the Irish Guide Dogs Day through to our own Open Banking Terminal. These are exciting developments, both for us as a company or enterpise, but also within the larger Open Banking sphere. However, quite understandably, the concept of Open Banking and Fire Open Payments is still an unknown to the vast majority. That is the inspiration for this blog post – to shed some light around the Fire Open Payments journey and, hopefully, prompt more of you readers to consider trialling the process yourselves!

The Open Banking journey with Fire Open Payments

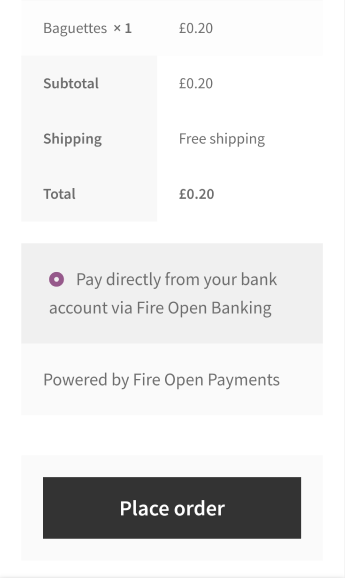

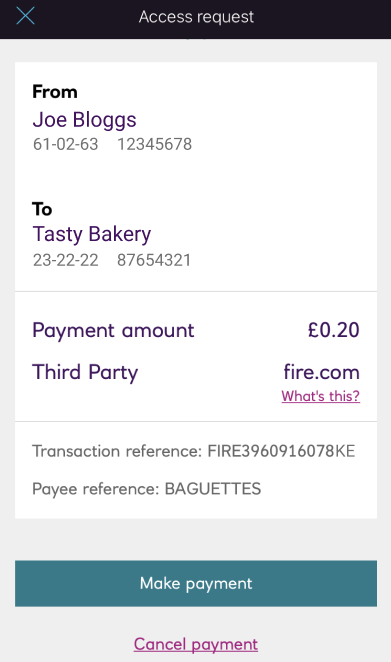

For this particular journey, I am on an e-commerce website and want to purchase a baguette from my local bakery – Tasty Bakery.

Similar to any e-commerce flow I select my products, and go to the “Checkout”. After entering my Delivery Details I then proceed to payment. At this point most of us would be used to fumbling around for our purse/wallet, then squinting to transcribe the card number into the website.

However, with just a tap of a button, I am redirected to the Fire Open Payments journey.

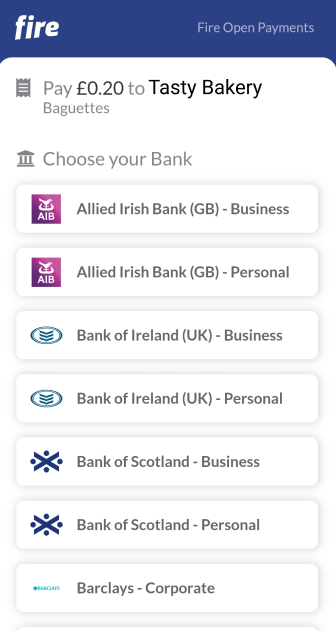

I select my bank of choice from the list.

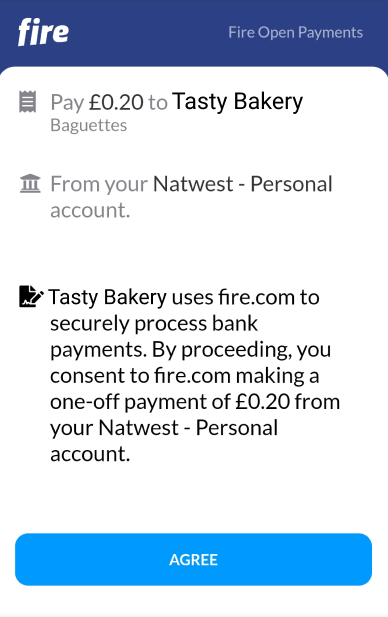

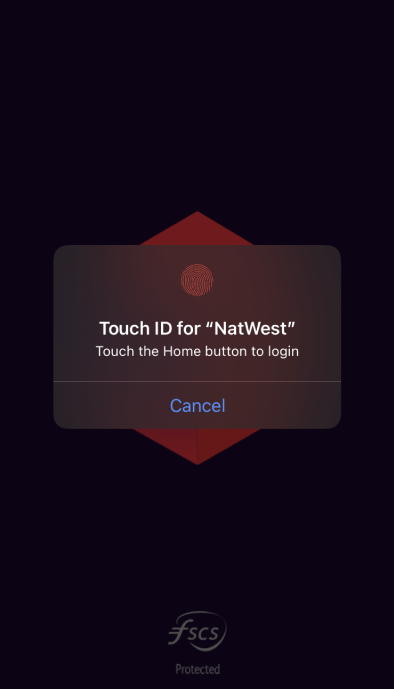

I bank with Natwest, so I’ll select them from the list. I then consent to the payment, which will redirect me to my Natwest banking app.

I will be prompted to log in to my Natwest app to authorise the payment. This part of the journey will be dictated by the bank itself in terms of how it designs their app flow.

This is an important part of the journey; it ensures that the customer who initiated the payment is the account owner and not attempting to make a payment fraudulently.

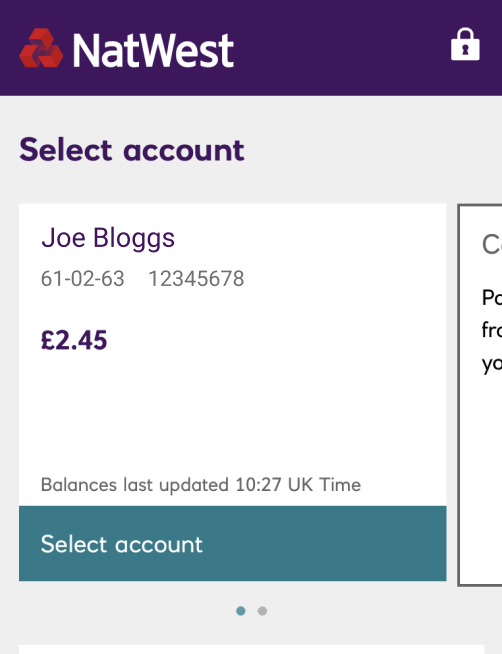

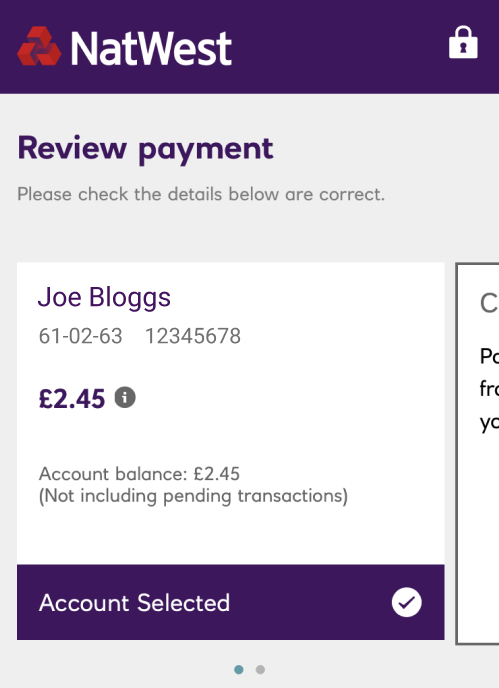

After scanning my fingerprint, I select the account I wish to pay from.

A quick tap of the ‘Account Selected’ button and I can authorise the payment.

Thankfully my account balance just stretches to cover the payment and I will be able to complete the purchase!

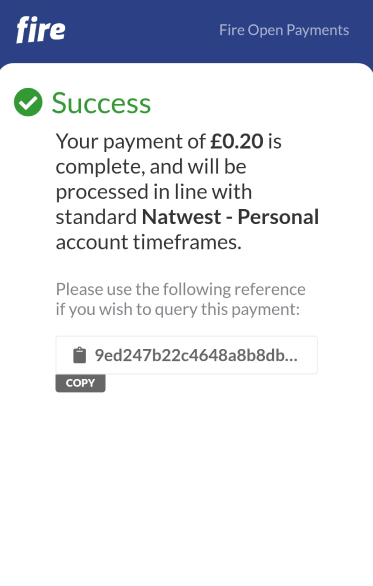

I will then be returned to my browser where I see that the payment has indeed been successful. I can request an optional receipt before returning to the merchant website, where I will hopefully be informed that my baguette will be delivered fresh from the oven.

Conclusion

There you have it, I’ve managed to make a payment through Fire Open Payments. The main benefits to my mind is the flow itself and the enhanced security. I never had to divert my attention from my phone to complete the payment; everything is contained within my browser and banking app. Having the flexibility to choose the account to pay from, coupled with a live view of my account balance was a bonus too.

This process provided that added assurance by authenticating the payment using my fingerprint – I was confident that no one could fraudulently create a payment on my behalf without access to my thumb! Also, if you’re security-conscious like me, I never save my card details within the browser, so I regularly find myself leaving the comfort of my couch to retrieve my debit card to enter my card number. This step was completely bypassed through Open Banking.

If you are curious about trying the process yourself, scan the QR code below or head over to https://www.fire.com/donate to make a small donation to Calcutta Connect and trial the Open Banking experience.

The way in which merchants accept payments and the devices/terminals used to facilitate these transactions have undergone quite the evolution over the past 70 years. Merchant acquiring technology now comes in many form factors tailored to the business needs of each merchant case. Although, over this time cards have remained the primary payment method which consumers rely on. The introduction of open banking payments unlocks the potential for a new paradigm shift away from cards and towards account based payments. Merchants are beginning to realise the benefits that come with this new payment mechanism and consumers are becoming familiar with a new payment flow.

In this blog post we’ll:

Cover a brief background on the evolution of merchant devices and consumer payment methods.

An overview of open banking payments and the benefits they can provide to merchants.

Introduce the Open Banking Terminal by Fire – transforming your mobile device into a point of sale terminal ready to accept open banking payments straight into your Fire Business Account.

A Brief History of In-Person Payments

When looking back at the evolution of in-person payments we’re going to be focus specifically on the consumer payment method – how are funds exchanged between the merchant and consumer and how quickly does the merchant receive the funds?

Evolution of consumer payment methods over time

The primary consumer payment method by and large remained unchanged until the first big shift from cash to card payments with the introduction of the Diner’s Club charge card in 1950. Since then, we’ve seen card technology go through many iterations from the conception of the card networks in the 1950’s, the introduction of the magnetic strip in the 1980’s, EMV technology in the 1990’s and mobile wallets in 2008. All leading to more secure and accessible card payments. Although incremental improvements were made over that time the primary consumer payment method largely remained the same, a card payment. The same financial players are involved: issuers, merchant acquirers, card networks and numerous intermediary service providers. Open banking payments help facilitate the next big shift in consumer payment methods from card to account-based payments.

Open Banking Payments and its Benefits to Merchants

As covered in our previous blog post, “Open Banking Payments – What needs to happen next?”, open banking payments in the EU and UK can be traced back to the introduction of the second Payment Services Directive (PSD2) and it’s associated regulatory technical standards (RTS).

With these account based payments there are a number of benefits for merchants and consumers alike:

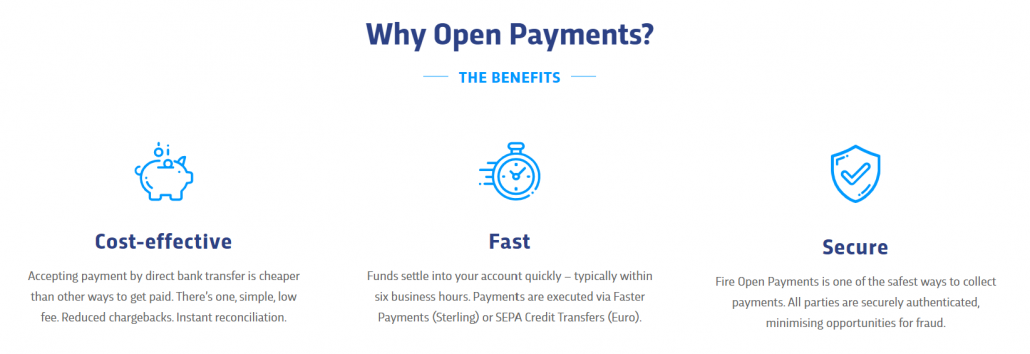

Cost-Effective – No hardware required. Accepting payments through the Open Banking Terminal is cheaper than other ways to get paid. No monthly or recurring fees, just one low transaction fee and reduced chargebacks.

Quicker Settlement – By executing payments via Faster Payments (Sterling) or SEPA (Euro), funds settle into your Fire Business Account quickly – within 6 business hours. Reconciliation is automated.

Less Fraud – The Open Banking Terminal is one of the safest ways to collect payments. No personal credentials are needed, reducing the risk of fraud.

The Open Banking Terminal by Fire

With the introduction of the Open Banking Terminal by Fire, merchants can realise the benefits of the shift towards account based payments from within the Fire Business Mobile App. Allowing any merchant to quickly accept ad-hoc payments from their customers on the go and have collect the funds straight into their Fire Business Account within 6 business hours.

Enter the amount to be paid in the Fire Business Mobile App.

A QR code is generated in the app to be presented to the customer to scan.

The customer scans the QR code and picks their bank.

The customer consents to the payment.

The customer are redirected to their Bank’s mobile app.

The customer reviews and authorises the payment from within their Bank’s mobile app.

The customer and the business receive confirmation that the payment was authorised and will be processed.

Check out our announcement video to see the full Fire Open Payments Terminal flow in action here.

fire.com is one of the UK and Ireland’s major Open Banking providers. To get your hands on the Open Banking Terminal by Fire and start accepting Open Banking Payments today, set up a free business account and download the Fire Business Mobile App today.

Jake McCarthy is a Product Analyst at Fire with experience across partner payment solutions, transaction monitoring and payment processing.

Open Banking was, at one time, set to give consumers access to their bank and e-money accounts with the ability to share information and initiate payments via regulated third party providers. It was a great ambition to bring competition, innovation and a new set of players into the market. It was envisaged that fintechs would bring new benefits to businesses and consumers, allowing secure ways of sharing information and making online payments. It would herald the end of screen scraping and move the industry to API based integration. There are countless benefits that these changes would bring.

A few years on, we find ourselves at a crunch point – a critical time for the era of open banking.

How it started

As a digital account provider, Fire are particularly interested in the payments aspect of open banking. In fact, our interest in open banking payments stems back over ten years. Fire was initially a part of a card based payment gateway business for online retailers called Realex Payments. Back then we set up Fire to be the “collections” account for retailers who wished to get paid when accepting payments directly from their customers’ accounts, rather than accepting cards. Account-based payments remain a major payment method in various countries across Europe.

The arrival of the second Payment Services Directive (PSD2) and its associated Regulatory Technical Standards (RTS) created the legal and regulatory environment for new account information (AISP) and payment initiation service providers (PISP). We became regulated for both account information and payment initiation services, knowing that account-based payments worked extremely effectively in other regions. We also could see that account-based payments were a preferable option for certain retailers to be paid by consumers.

Account based payments offer huge benefits for both retailers and consumers. These benefits include better security, less sharing of sensitive data, lower fraud, potentially lower processing costs and faster settlement times for payees (retailers). Driven by our experience and seeing the underlying value proposition, we set about building Fire Open Payments, an open banking payments solution for retailers to accept payments directly from their customer’s accounts.

How it’s going

In terms of how open banking payments are progressing, it’s a very different story in the UK and the EU. Fire operate and are regulated in the UK and the EU. At a recent UK Open Banking event, a speaker noted that there were as many TPPs active in the UK as there were in the whole of Europe.

The UK has become the undisputed leader in Open Banking. The creation of the Open Banking Implementation Entity, via the CMA, has led to the development of a coordinated approach by the nine largest UK account providers (ASPSPs). This gave rise to the creation of the first era of open banking in the UK. While It is by no means complete, the fundamental building blocks are solid. In addition, the ecosystem remains open and engaged. All stakeholders – from consumer groups, regulators, trade associations, account providers and TPPs are participating in healthy discussions about how best to shape the future. The possibilities for open banking payments remain very strong in such an ecosystem with numerous issues on the agenda, all of which are monitored by regulatory eyes.

In the EU and specifically in Ireland, where Fire is based, the adoption of open banking payments is at the other end of the spectrum. Open banking has not yet taken off. So what’s gone wrong?

To make open banking payments a reality, the ecosystem needs to see a standard implemented in a consistent way. This ecosystem should encourage account providers and third parties to interact and attempt to implement a customer experience that is not just compliant, but a frictionless experience. The UK outcome has clearly demonstrated that this is possible. The fact that the Irish market has not achieved the same level of success as the UK has nothing to do with regulation. The delay in implementing an acceptable user experience by some Irish account providers, when their customers are accessing their account via third parties, has had a serious and detrimental effect on Ireland’s open banking ecosystem. This has been a major barrier for fintechs to bring new benefits to businesses, consumers and the economy at large. The fact the the UK based customers of these institutions enjoy a better experience confirms that the capability exists and leaves us all to wonder why this situation has evolved. Meanwhile, Irish businesses and consumers are being denied the benefits of open banking payments. To put the situation into context, we had a client who was accepting open banking donations that had a conversion rate of 4% with one Irish bank.

What to do next

In terms of what should happen next, we see the UK and Irish markets with a different set of priorities.

In the UK there is recognition of the excellent work completed to date, along with a sense of reality that we are still at the early stages in the development of open banking payments. With the CMA order coming to a rightful close, a transition period will need to be managed as a new entity emerges to carry on the work of the OBIE. This process is currently underway. In addition, specifically in relation to payments, we see this as an opportune time to identify and discuss any barriers and accelerators that could fuel the adoption of open banking payments. Issues such as fragmentation of the market, API uptime, implementing a decoupled experience, devising limits for open banking payments akin to contactless payments, enhancing the exchange of data at payment initiation time to assist with fraud and how variable repeat payments could be rolled out to the full ecosystem and apply to more use cases. These are great topics to be discussing as they all build on what is already in place. We believe the other aspect of open banking payments in the UK that needs consideration is the status of the payment pillar within the new entity. The concept of this being a “Payment Arrangement” is worth examining as it could help to ensure that there is a governance and operating model that is inclusive of all players. This would mean that open banking would have the appropriate level of regulatory oversight.

For the Irish market, there are different actions that we would suggest. Given that the market is behind in its development, we believe that some policy oversight is required. As things stand, TPPs have no indication as to when the issues will be addressed, rendering market and sales planning a fruitless exercise. Leaving the market to sort itself out will delay the delivery of a vibrant open banking ecosystem and continue to deny businesses and consumers the benefits of cheaper, faster and safer payments. Unlike the UK, the Competition and Consumer Protection Commission (CCPC) in Ireland has not issued any remedies to address the issues. However, such action may not be necessary if the CCPC, the Central Bank of Ireland (CBI) and the Department of Finance were to coordinate a forum and express their clear expectations with respect to the development of open banking payments in Ireland. Such an action would be the first step and could potentially be sufficient to address the issues. The problem is, who will take the first step?

Photo: Roy Keane launches Irish Guide Dog Day (Friday 7th May 2021)

As Irish Guide Dogs for the blind launch their annual Guide Dog Day, we see Fire Open Payments / Account-to-Account Payments in action.

Fire.com are delighted to assist Irish Guide Dogs for the Blind with their annual Guide Dog Day. Guide Dog Day is a major annual charity event in Ireland that focuses on raising funds and awareness for the organisation. Starting this month, Irish Guide Dogs are using fire.com’s Open Banking payments solution that allows people to donate directly from their bank account with no card required. Try it out below by scanning or tapping the QR code!

Irish Guide Dogs will receive 100% of donations made through Fire Open Payments. For now, we recommend using Revolut, Fire, Bank of Ireland or Ulster Bank when making a payment; AIB expect to update their approval flow over the summer.

Scan or Tap the code to donate to the Irish Guide Dogs using Fire Open Payments.

Fire’s CEO, Colm Lyon, had the following to say:

‘We are delighted to be working with Irish Guide Dogs and helping them to accept donations directly from peoples’ bank accounts. It’s such a simple and easy way for charities to accept donations – no card details to be entered, just tap or scan a QR code and approve the payment. It’s a great moment to see such a leading charity embrace a new and innovative way to accept donations.’

Fire Open Payments is available to charities or any organisation who wishes to accept payments via Open Banking.

What is Fire Open Payments?

Open Banking Payments are account-to-account payments that are initiated by the Payment Service Provider (PSP) directly from the customer’s bank account to the merchant’s bank account. In this case, fire.com is the PSP and the merchant is Irish Guide Dogs.

The core of Open Banking is based on customer consent. Open Banking allows customers to initiate a payment using their mobile banking app or online banking web portal. Funds are then transferred to the merchant using strong customer authentication without the use of a debit or credit card.

When making a payment, it is as easy as:

Select your bank from the list.

Authenticate with your bank and authorise the payment.

You’re done!

If you’re interested in adopting Fire Open Payments as a payment method for your organisation, check out our Open Payments Page here or feel free to contact us directly.

Where does my Donation Go?

Irish Guide Dogs will receive 100% of donations made through Fire Open Payments. With the payment QR code above, you can choose how much you wish to donate.

By supporting the Irish Guide Dogs for the blind, you are directly supporting them to meet a growing demand for their services as the organisation costs €5 million to run each year! The Irish Guide Dogs have shared their yearly progress with us.

2021 Irish Guide Dog progress:

Breeding Programme continues to grow with 3 litters successfully born so far this year

105 puppies currently being puppy raised. These pups will be the dogs who start formal training later in 2021 and during 2022.

39 pups currently undergoing formal training who will hopefully be successfully matched in the coming months.

Assistance Dog Programme waiting list due to open later this year or early 2022 (subject to COVID-19 restrictions).

Photo: Irish Guide Dog’s new Dog Bandana

Further Information on Irish Guide Dogs

Irish Guide Dogs for the Blind is a national charity dedicated to helping people living with sight loss or autism improve their mobility and independence. For over 40 years Irish Guide Dogs have provided life-changing services and support to people across Ireland with sight loss. All services are offered free of charge and include the following:

The Guide Dog Programme for people who are blind or vision impaired

The Assistance Dog Programme for families of children with autism

The arrival of Open Banking Payments (also known as account-to-account (A2A) payments) is already starting to shift the way consumers and businesses pay and get paid. Regulated third-parties such as Fire are enabling Open Banking payments directly from a customer’s or donor’s bank account to a businesses or charities account. Open Banking is shaking up an industry that has historically been difficult to access – inviting more competition and stimulating innovation.

The figures are starting to back up the hype in the Open Banking payments space. Figures released by the Open Banking Implementation Entity in the UK show how this growth is beginning to really take off in 2021. In 2018 there were 320,000 Open Banking Payments made, and in just 2 years this figure has grown by over 1,000% to 4,000,000 Open Banking payments in 2020 and over 1,000,000 in February 2021 alone.

Given this shift by merchants and customers towards using Open Banking payments a question that often comes up from merchants is “how can I accept recurring payments using Open Banking”. This is to be the next big development for Open Banking in the UK and is called “Variable Recurring Payments”.

If you work outside of the FinTech sector, chances are you have not heard of Variable Recurring Payments before, however, with the key financial, access and control benefits to both consumers and businesses alike, it is worth familiarising yourself now.

Variable Recurring Payments (VRP) Overview

So, what are variable recurring payments and how are they different to card-on-file and direct debit solutions that businesses already have in place?

In short, Variable Recurring (or VRPs) are a new way of making payments using bank APIs, and are a cheaper and more secure alternative to Direct Debits and card-on-file for recurring payments. VRPs allow an account-holder to give permission to a regulated third-party provider to make payments from their account based on restrictions such as payment amount and number of payments allowed. VRPs could be used instead of card-on-file for Netflix, Spotify or Amazon purchases or instead of a direct debit for recurring donations to a charity. One of the first use cases that may be available will be ‘sweeping’. Sweeping is where funds are automatically transferred betweentwo accounts of the same name (e.g. to automatically move money to or from their current account to avoid overdraft fees or to transfer to savings or pensions). VRP is particularly well suited for sweeping as the transfers are quick, cheap and secure as opposed to using cards which can be expensive or direct debits which are too slow.

The main advantages of VRP from a customer perspective is that these payments have tight limits that are setup by the customer using a “consent”. From the business or service provider perspective it gives them a cheaper, faster way to get paid than card-on-file or direct debits that also leaves them less exposed from a risk perspective as they can not accidentally bill the customer for a larger amount than intended, longer than intended and there are also no sensitive card details that can be stolen.

For example, as opposed to a customer giving a business their card details and losing control of how much and how long they can be billed, Variable Recurring Payments allow the customer to set limits on the payments via consent parameters. These consent parameters or limits provide control to the customer by allowing them to set the max amount per transaction, max amount per day, max amount per month, a time limit on the consent etc.

Examples of VRP Consent Parameters:

The maximum cumulative value of payments initiated under the VRP Consent

The maximum cumulative number of payments initiated under the VRP Consent

The maximum payment value per payment

The maximum cumulative payment value per time window

The maximum frequency of payments per time window

Expiry Date of the VRP Consent

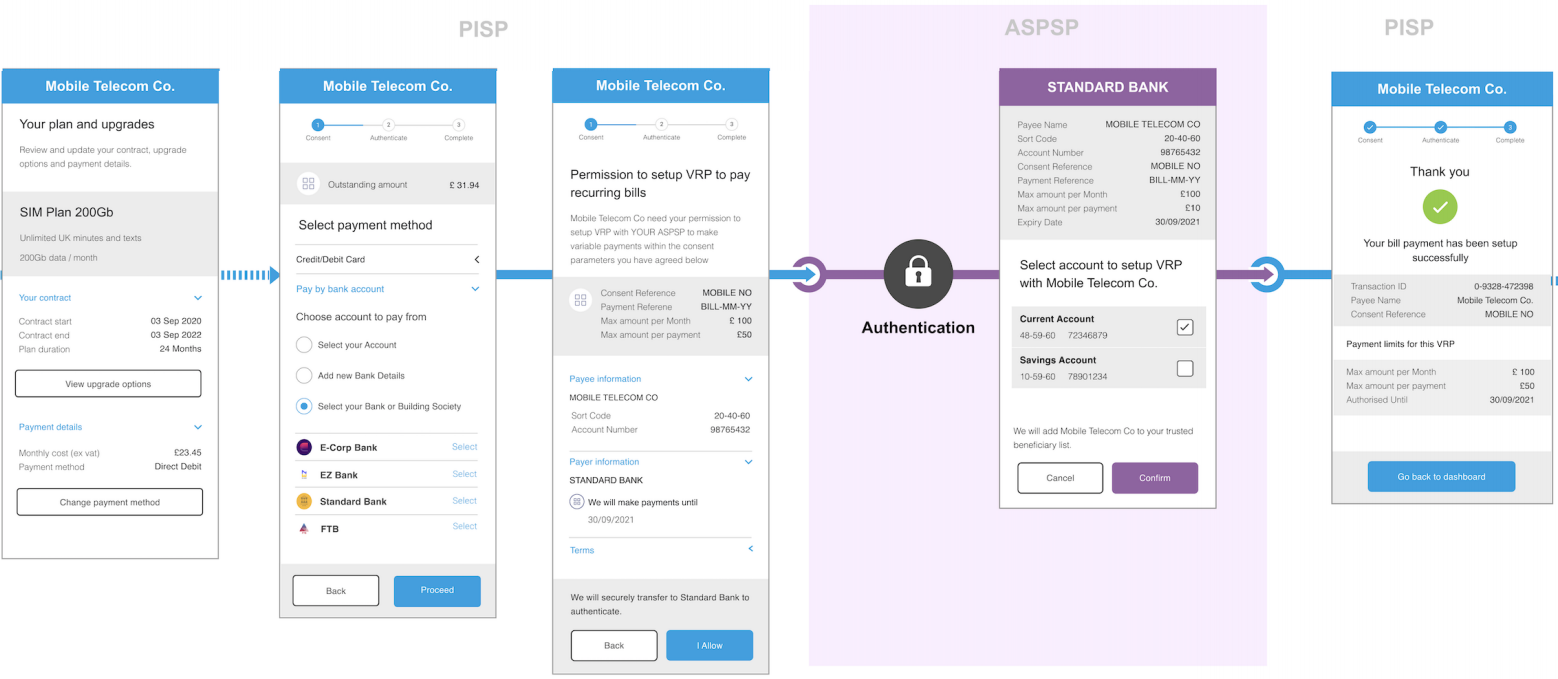

The user experience when setting the “consent” with the business using a third-party provider such as Fire would look something like this.

As a home owner, I want to allow my electricity provider to automatically take payments from my bank account but only up to a maximum of £100 per month.

As a user of a social network, I want to connect my bank account so that I can make quick and easy in-app authentication of payments to my friends and be able to easily disconnect it from an access dashboard with my bank if I change my mind.

As a new customer of a subscription service, I want to set up my subscription payments such that it expires after 6 months so that I don’t get caught in a subscription trap.

As a ride-hailing app customer, I want to connect my bank account so that payment is made automatically on my behalf as I arrive at my destination with a maximum payment size of £45.

As a customer using an online marketplace, I want to do a one-time payment setup for oneclick payments offered by the marketplace to enable a quick checkout process

As a customer looking to earn more interest, I want to use a third-party smart saving app that moves money from my bank accounts to my own saving account on a flexible/variable basis so

that I can save money.

As a customer looking to avoid unnecessary fees, I want to use a third-party service that monitors my account to maintain a threshold balance in my account or avoid overdraft fees and moves funds as and when required between my accounts.

As a customer in financial difficulty, I want convenient short-term credit to avoid going overdrawn, and then to automate repayments so that I minimise both my overdraft fees and

borrowing costs.

When will I be able to accept Variable Recurring Payment for my business?

The Open Banking Implementation Entity (OBIE) in the UK carried out a consultation earlier this year around VRPs and Sweeping. The aim of this consultation was to try and establish the next steps forward around giving access to third-party providers such as Fire to Variable Recurring Payments and also around using VRP as the preferred method for Sweeping on behalf of customers. The consultation looked at how this would look from an access, commercial, consumer protections and legal perspective. The OBIE recommendation was that VRP was the most suited method to carry out Sweeping.

There is currently no obligation for banks to provide access to third-party providers such as Fire to these APIs for VRP outside of Sweeping activities from a regulatory perspective. Access for VRP activities would currently still need to be agreed on a bilateral basis between the third-party provider such as Fire and the bank. This is something that we expect to change into the future.

The OBIE recently published their latest API standard version 3.1.8 on the 31st March 2021 which enabled both Variable Recurring Payments and Sweeping functionality. It is worth nothing that this standard is an optional standard that must be implemented by the CMA9 in the UK for access to Sweeping activities. VRP and Sweeping are very tightly coupled together from an Open Banking perspective. Sweeping was mandated by the original CMA order and roadmap whereas VRP was not. The OBIE have created an optional standard for VRP (API standard version 3.1.8 mentioned above) and have also carried out an evaluation and have concluded that the CMA9 should provide this VRP standard to provide for Sweeping access. This will effectively make it mandatory for all of the main CMA9 banks in the UK to provide access to Sweeping using the VRP APIs which opens their doors to allowing third-party providers full access to carry out all VRP activities once new regulatory or commercial access models are agreed. There is still a bit to go with some issues to be ironed out before customers will be able to pay their Netflix and Spotify using VRP as opposed to card-on-file but this is a big step in the right direction.

This new version of the API will allow companies such as Fire to access the bank’s APIs and initiate VRP transactions once the access, commercial and legal frameworks have been agreed, hopefully towards the end of 2021 or early 2022. The discussion around VRP is confined to the UK for the moment, as the EU are behind due to the lack of a EU regulatory mandate for banks to offer VRP or Sweeping access. Fire will keep you updated around the latest developments in Open Banking, Variable Recurring Payments and Sweeping.

While we wait for VRP and Sweeping to become a reality, Fire Open Payments is Fire’s Open Banking Payments product that can be used for one-off payments for your business. You can find out more about Fire Open Payments and try it yourself by reading our previous blog – The Steady Rise of Open Payments.

Discover the Benefits of Open Payments for your Business

Open Payments are hitting the mainstream – it’s time to look at adopting the new payment technology

Open Banking Payments are quickly disrupting the way we make payments online. By giving regulated third-parties secure access to financial information, it is shaking up an industry that has been difficult to access – inviting more competition and stimulating innovation.

‘More than 3 million people and businesses are using Open Banking-enabled apps and services in their daily lives.’

‘We’re beginning to see growth in Open Banking Payments. In 2018, 320,000 Open Banking Payments were made. This rose to over 3.4 million in 2020. In 2021, this has jumped dramatically, rising to 1.2 million monthly Open Banking Payments in January alone.’

As part of this shift, many are asking, what are open payments? This term refers to the innovative, direct transaction methods emerging under Open Banking.

Open Banking Payments are account-to-account payments that are initiated by the Payment Service Provider (PSP) directly from the customer’s bank account to the merchant’s bank account.

The core of Open Banking is based on customer consent. Open Banking allows customers to initiate a payment using their mobile banking app or online banking web portal. Funds are then transferred to the merchant using strong customer authentication without the use of a debit or credit card.

When making a payment, the customer can opt to pay by Open Banking if the business enables the new payment method. When you select to pay by Open Banking at the checkout, it is as easy as:

Select your bank from the list.

Authenticate with your bank and authorise the payment.

You’re done!

Want to try for yourself? Scan the QR code below on your smartphone camera or head over to www.fire.com/donate to make a small donation to Calcutta Connect to trial the Open Banking experience.

Why Should I Adopt it?

Open Banking Payments are both more cost effective and secure than a regular online payment for everyone involved in the transaction. It has been found that Open Banking Payments can be up to four times cheaper than card payments. The funds are also settled quicker than a typical card payment getting businesses their money sooner – it’s win/win for all parties involved.

Open Banking Payments also leverage new technologies such as making a payment via a QR code or URL link. For example, you can place a QR code on a menu, poster or even a website and the customer can pay by scanning the QR code on their smart device. Alternatively the customer can click on a URL link to take them to the payment page.

As the COVID-19 crisis has sped-up the development of online payment technologies, we are beginning to become a card-less society. Open Banking is at the forefront of this revolution and we are already seeing a huge surge of adoption here in Fire.

Lastly, it’s super easy to set up Open Banking Payments for your business with fire.com!

How do I Adopt Open Banking into my Business?

Fire.com is one of the UK and Ireland’s major Open Banking providers. In order to accept Open Banking Payments into your business, setup a free Fire.com business account where you can create new Open Banking Payment requests and integrate them with your business.

Initiate large volumes of bank transfers to any account in the UK or eurozone from your internal systems.

Embed account and transaction information in your inhouse systems, developing better financial control applications.

Receive event driven data from Fire, e.g. when a payment is received, so you can update your systems and reconcile faster.

Additionally, Open Banking is a great asset for those managing freelancer business accounts. Its streamlined and secure payment processes are particularly advantageous for freelancers, who often navigate multiple transactions and client relationships, offering them a more efficient way to handle their banking needs.

Moreover, Fire.com’s Open Banking services extend beyond individual and small business solutions, evolving into a comprehensive enterprise payment platform. This platform is designed to cater to the complex and varied needs of larger enterprises, offering scalability, enhanced security, and a range of features that are essential for high-volume transaction management.

In an online retail setting, cart abandonment is when a shopper shows interest in a business’s products or services by adding items to their cart, but do not complete the purchase. Cart abandonment rate is calculated by dividing the total number of completed transactions by the total number of opened carts. Currently, the average cart abandonment rate is 69.57% across e-commerce industries, meaning almost two thirds of considered purchases are not completed.

With such a large percentage of potential purchases abandoned, e-commerce merchants are continually seeking out new ways to reduce abandonment and increase conversion. The good news is that some of the most effective fixes are simple to carry out. Here are five strategies you can implement quickly, to help minimise your website’s cart abandonment rate, simplify your checkout experience and boost your bottom line.

1. Reduce user experience (UX) complexity

To help your customers find their way, you should ensure your website’s end-to-end customer journey is streamlined with effective navigation guides. A/B test the colour and placement of call to action (CTA) buttons and experiment with different graphics, product images and designs in order to determine what combinations yield lower cart abandonment rates.

A range of CTA buttons of different sizes using different fonts and colours. (Image source).

Look to minimise the number of clicks required to reach the end of the customer journey. Once the shopper is in the cart and has indicated they want to buy, the information they are presented with should encourage them to continue with the payment journey. Consider limiting the buttons or links that route to other parts of the website during the final part of the payment flow.

2. Offer multiple payment options

Have you ever gotten to the checkout on a website, filled in your address and details only to discover you can’t pay, as the retailer doesn’t accept your preferred payment method? A recent article in Forbes notes that out of 1,799 of online shoppers surveyed, 8% admit to abandoning a shopping cart because there weren’t enough payment options (2019).

E-commerce merchants can avoid losing customers by diversifying their payment acceptance methods. One way to achieve this is by adding Open Banking or ‘Pay by Bank Account’ functionality to your e-commerce payment page.

Open Banking is a new way to accept payments than can be used to supplement card payments. The customer is redirected via the shopping cart to pay directly from their mobile banking app or online bank account. There’s no data entry (such as card numbers or IBANS) required, payments settle quickly (typically within six business hours), fees are typically low for online retailers and it is more secure than other ways to get paid. Open Banking providers such as Fire are integrated with every major bank account provider in the UK and Ireland, meaning shoppers with access to an online bank account will be able to pay directly from their banking app. Open Banking payments can also be integrated with existing e-commerce systems for a fully integrated payment, reconciliation and returns process.

For further insights on optimising your e-commerce strategies , our Business Banking FAQs can provide comprehensive answers and guidance. This resource is tailored to help businesses navigate the complexities of digital payments and enhance the efficiency of their financial operations.

3. Simplify the payment authentication process

Recent changes to Strong Customer Authentication (SCA) mean online merchants are now responsible for ensuring payments made on their website are authorised and authenticated as per the European Union’s Regulatory Technical Standards. This means that if you want to accept payments online, you need to build additional authentication into your checkout flow. The additional authentication must be two of these three identifiers: something the customer knows (i.e password), has (i.e: mobile app) or is (i.e: biometrics).

Some payment methods, such as Open Banking, have a simple SCA process as the authentication forms part of the payment flow. For card payments, authentication may involve the shopper being temporarily redirected away from the payment flow to receive a numerical code via SMS or being asking to open their mobile banking app to approve the transaction. This can add friction to the payment experience and potentially increase abandonment rates.

4. Experiment with hidden cost pricing and transparency

Shipping costs and fees are an essential part of online shopping and significantly affect conversion rates. Delivery options, including carriers, delivery times and shipping costs all affect whether a customer proceeds through to checkout. According to Statista, in 2018, 63% of online shoppers abandoned their carts in 2018 due to high shipping costs. Furthermore, in a 2020 study by BayMard Institute spanning several years of statistics, extra fees like shipping were the top reason shoppers called it quits on a purchase. To avoid cart abandonment due to hidden costs, you may wish to experiment with incentives such as free delivery above a certain transaction value. Or if incentives are not profitable, consider being upfront with hidden costs at the start of the customer journey to increase the quality of your leads.

5. Collect regular feedback

One of the most important strategies to reduce cart abandonment rate is a corrective feedback loop. This doesn’t have to be complex and could include a short survey sent to a GDPR-compliant list of customers who have previously engaged with your products and services to find out how they found your website’s end-to-end UX. When it comes to designing an effective and delightful customer journey, you will never get it right first time. It’s all about iterative improvements, regular feedback and rapid testing.

Shopping cart abandonment is a major source of potential revenue loss across the e-commerce industry, however by making a few simple changes to your customer journey you can lower your website’s rate with relatively low effort. By reducing the number of clicks in the buyer flow and cutting complexity in design where possible, the proportion of leads that convert may naturally increase.

A key consideration is the payment page – it’s important to have a range of payment acceptance options available and ensure payment is as frictionless as possible. This could be achieved by adding Open Banking payment functionality to your checkout, giving online banking customers in the UK & Ireland the ability to pay quickly and securely with no clunky authentication process.

Online retailers may also benefit from testing with hidden cost transparency and incentives and implementing corrective feedback loops to inform continuous improvement.

Getting started with Open Banking

You can try out accepting payments by Open Banking on your website by opening a Fire Business Account today with no set-up cost or fixed fees. Once your account is live, simply generate Open Payment Request Links in your account manually and use them to invite your customers to pay with an account-to-account transfer. Use the links to create website buttons, QR codes, social media ads and more – the payment request is a URL so when it comes to presenting it to your customers, there are many options.

Fire also has a full API, so Open Banking payments can be integrated with existing systems and automated in, out and reconciled as required. Out-of-the box options, such as Shopping Cart Plugins for e-commerce platforms like WooCommerce are available to make integrating Open Banking payments simple, with no extra development required.

About Fire

Trusted. Digital. Payments.

The Fire Business Account helps businesses of all sizes access payment services and automate payment processes. With our technology, API and regulatory licences, Fire delivers solutions that make payments faster, more cost effective and secure. Discover our payment platform at fire.com

Have you recently started a business or are you self-employed and looking to open a business bank account? We answer frequently asked questions by freelancers to help you make the right decision as you shop for a new account provider.

Can I use my personal account instead of a business account?

If you are a sole trader, you may use your personal account for business purposes, depending on what provider you use, but it is not recommended for a number of reasons (see question 2). If you are a limited company, you must have a business account.

Why shouldn’t I use my personal account for business use as a freelancer?

Your bank or provider’s T&Cs It is likely your account provider has stipulated that your personal account should not be used for business purposes in its T&Cs. If it is clear you are violating these terms, your account could be closed.

It makes calculating your tax return tricky If your personal and business costs are mixed up, it can make it difficult to calculate how much tax you owe at the end of the financial year.

Brand reputation and trust Having clients pay into a business account and seeing your company name come up as the payee looks more professional. Some clients may not feel comfortable paying into a personal account.

Why should I open a business account as a freelancer?

Enhanced visibility over your business finances With a business account you can see at a glance what you’re spending, how well you are doing, and manage your business more effectively. With this increased visibility, it will be easier to deduct business expenses as you fill out your annual tax return.

Access more suitable features Some business accounts may offer better fit features, such as the ability to process batch payments, export data compatible with accounting software or order business debit or credit cards.

Prime your business for growth Opening a business account is the first step towards a finance system that is built to scale. If you want to grow your business, it is better to have the correct systems in place from the off than to return a few years later when issues may have grown.

To ensure you’re making the most informed decision, we highly recommend checking our Business Banking FAQs. These FAQs provide valuable insights into various aspects of business banking, helping freelancers and self-employed individuals navigate their financial options with greater clarity.

What is the easiest business account to open as a sole trader in Ireland?

There are a number of account providers available to freelancers in Ireland. Broadly speaking, these can be split into high street offerings and challenger bank offerings.

If by ‘easier’, the implication is ‘quicker’, often the speediest way to open a business account is via a challenger bank. These providers are more agile and often have faster onboarding processes. They may also offer account features that high street banks do not.

What documents do you need to open a business account?

Before opening your business account the provider may need to run a Know Your Customer (KYC) check on you. These checks are to prevent fraudsters from using their account services for illegal purposes. To prepare for a KYC check you should have to hand at least a form of identification, proof of business activity and address. Required documentation can vary depending on the provider.

I want to open an account today, how do I do this?

You can apply for a Fire Business Account online today at fire.com. Once the team has approved your documentation your account will typically be live within two working days.

Why should I opt for a Fire Business Account?

From Mastercard® debit cards and bank transfers to a host of API services, a Fire Business Account gives you all the features of a premium business account – but with so much more:

Open any number of Sterling and Euro accounts

With a Fire Business Account you can keep various parts of your finances separate in segregated Euro or Sterling accounts. Easily silo VAT and expenses.

Order as many debit cards as you need

Get access to your own business Mastercard debit card. Order more cards for your staff as you grow and block and unblock in real-time.

No set-up costs No fixed costs, no recurring fees, no hidden charges and no surprise bills. At Fire we provide clear transparent pricing, meaning you always know how much a transaction will cost. We’ll deduct the transaction fee when it happens, so you only pay for what you use, when you use it.

Access a full suite of payments services From Faster Payments, to SEPA, to direct debit, 24×7 FX and Open Banking (Get Paid by QR Code) features, Fire is constantly adding new payments services to its Business Account offering.

Reports compatible with accounting software Export data compatible with leading accounting platforms including Xero, FreeAgent and Sage. Reduce time spent and mistakes made when calculating your accounts.

Integrate and build

A Fire Business Account is the account that grows with your business. As you scale, you may require an account provider that offers API services to allow you to automate your payment processes, saving time and money. Fire has a full API used extensively by medium-to-enterprise clients for splitting and sweeping funds automatically – and for integrating with third-party systems.

At Fire, we work closely with freelancers, self-employed people and small business owners to help them manage their finances using a Fire Business Account. The account’s unique features enable them to effectively monitor expenses, ring-fence tax, automate reconciliation and utilise accounting software. To find out how a Fire account could benefit your business, get in touch with our team.

How digital advertising agencies can simplify their payment workflows with client-specific accounts and debit cards.

Managing a high volume of payments for many different clients at the same time, makes sorting and reconciling payments particularly challenging for PPC agencies.

The pain of getting paid in PPC

PPC payment collection workflows differ depending on the provider’s pricing model – which can range from hourly rates, to percentage of ad spend, to performance-based pricing. However, in any PPC pricing framework, a line of credit may need to be extended to clients up to a month in advance. As the costs involved in PPC advertising can be significant – up to £/€20K per month per corporate client, depending on the industry – the risk absorbed by the provider can be considerable.

Another common payment problem arises when campaigns owned by different clients draw funds from the same business account, using the same debit card. Reconciliation – which is often manual – becomes a highly resource-intensive process. In instances where there is a payment issue, such as with a late payment, it can take time to identify the root cause of the problem. This is particularly the case when there are many clients paying into the same account.

Segregate and Simplify with a Fire Business Account

With Fire, PPC agencies can now open separate business accounts for each of their clients with no further administration. New accounts are opened via the parent account at the account-holder’s request. Each account comes with its own IBAN or Sort Code and Account Number, depending on if it is a Euro or Sterling Account, while debit cards can be ordered in any number, with transaction limits to suit your needs. As you can change which account the debit cards link to from within your account, you can easily charge campaigns to the correct account using any Fire debit card.

Fuad Aliyev, Director of AfeaGroup, a leading advert digital advert agency and ad budget analyser said of the service: “We use Fire for our clients’ digital ad campaigns and are very happy with the service. Incoming and outgoing transfers are smooth and their debit cards have generous daily transaction limits. This is a useful service for digital ad agencies that need to use a different payment profile for each of their clients – especially for larger clients.”

Using segregated accounts, reconciliation is made easier for PPC agencies and identification of a late payment, or other payment issue, is often faster. The client is given their unique details, so they can pay in instalments over the course of the campaign or along an agreed timeline. As the service provider, you absorb less risk and the value of the credit needed to be extended to the client is reduced.

A Fire Business Account is quick to open and there are no set-up costs. It can be used by PPC agencies to segregate and simplify their payment workflows, with no development needed. For those requiring integration with existing systems or an automated system, we have a number of API Services.

You can register your interest for a Fire account here. To speak to one of our team about how the account could work for your business, get in touch.

The last thing you need when you are trying to run a business is uncertainty about the future of your eurozone payments. Maybe you have been informed by your existing account provider that your euro accounts are being converted to hold accounts only accessible by SWIFT transfer. With Fire’s dual regulation in the EU & UK, you can open an account and use any of Fire’s card or payment services and be assured your access will not change as Brexit becomes a reality.

Trade into the eurozone easily with a Brexit-ready dual-currency business account

Fire is authorised as an e-Money Institution by the FCA in the UK and regulated as a Payments Institution by the CBI across the EU. UK and Irish businesses can benefit from a range of payments services and business accounts with individual account numbers & sort codes, or IBANs.

Helping businesses get paid in Sterling and Euro

1. Open as many Sterling and Euro Accounts as you need

Open Sterling and Euro accounts to manage payments and simplify reconciliation. Create additional accounts in real-time. Use them to segregate funds, simplify reconciliation processes or manage projects and expenses. Pay and get paid by bank transfer to and from any bank account in the UK or Eurozone, and avail of Fire’s instant, low cost FX service to manage the currencies.

2. Order debit cards for all your staff

A Fire debit card is linked to both a Sterling and Euro account, so you automatically pay from your Sterling account when transacting in Sterling and from your Euro account when paying in Euro, avoiding unnecessary bank fees.

3. Automate your payment processes

Use the Fire API to integrate internal business systems or applications directly to your accounts and cards. Automate pay-outs, streamline payments in, instantly reconcile, split funds and more.

4. Accept Open Banking payments

Sell online or via social media with payment links and QR codes. Get paid directly from your customer’s account via Open Banking Payments, without the need to accept cards.

5. Put your business in safe hands

Regulated in the EU and UK and licenced to provide payments services for more than ten years, Fire is a member of numerous payment schemes and networks. We are a team with decades of payment expertise and experience and some of largest financial institutions in the world work with us. Fire is a principal issuer of Mastercard® debit cards and an approved provider of Faster Payments, Bacs, Direct Debits, SEPA and Open Banking. All client funds are segregated, ring fenced and held with tier-one financial institutions, in line with UK and EU legislation.

If you are considering opening a business account, or are concerned about the continuity of services from your current account provider after 1 January 2021, please don’t hesitate to get in touch with our team to discuss your options.